What’s Behind Today’s Crazy Market Move

BY TYLER DURDENTHURSDAY, JUN 17, 2021 – 05:44 PM

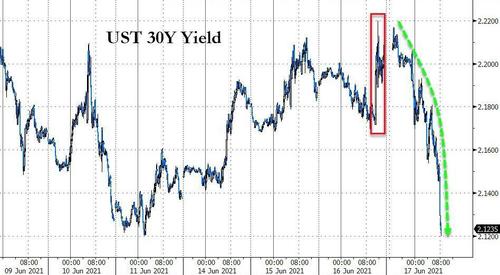

One day after the shockingly hawkish Fed admitted that inflation is not, in fact, transitory as so many clueless propaganda hacks would want everyone to believe, and pulled up the liftoff date to early/mid-2023 when it now envisions not one but two rate hikes, traders are watching in stunned amazement at what is going on in the market where contrary to everything the Fed has said, we are seeing a stampede into tech, growth and duration-sensitive names…

… and a flight out of reflation and value sectors…

… while bonds are crazy bid, a 180 degree reversal from yesterday’s market reaction.

What’s going on here? Did Powell secretly announce to his favorite accounts (a la the ECB) that he is really doubling down on QE even as he tells the peasants that he is preparing to tighten.

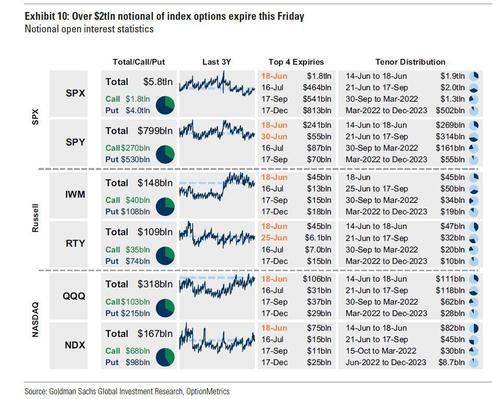

Nope, and in fact the answer to day’s move is found not in what happened yesterday but what will happen tomorrow, when as a reminder, we get a massive quad-witch when over $2.2 trillion in index option gamma is set to expire.

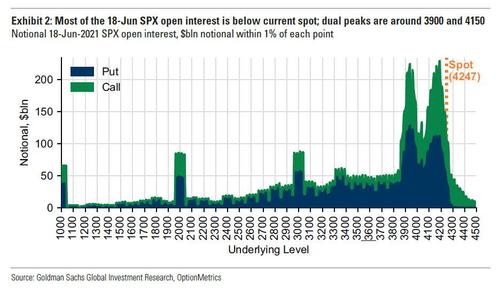

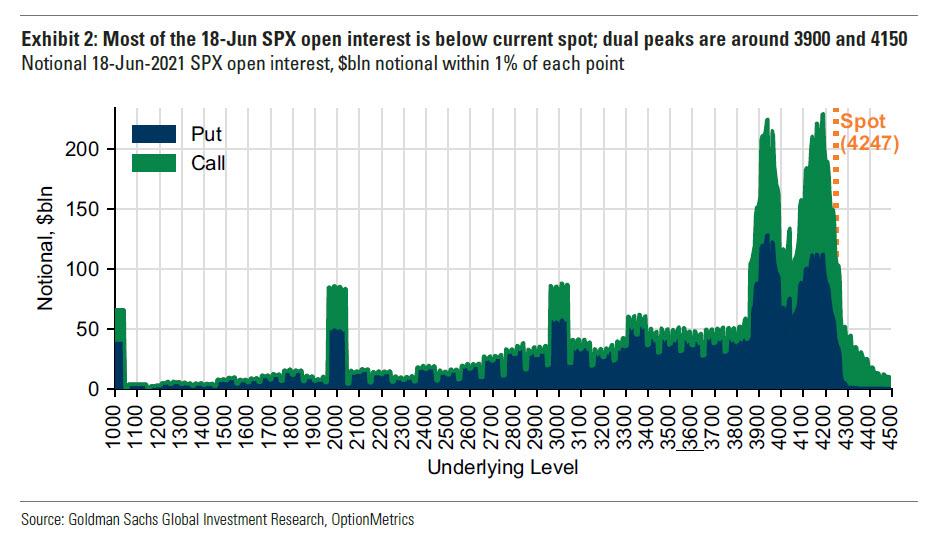

As we discussed earlier this week, according to Goldman estimates Friday’s opex account for around 20% of all SPX options. Furthermore, with stocks at all time highs, it is to be expected that most of the June open interest is below the current SPX spot price. As shown in the chart below, the dual peaks are at 3,900 and 4,150. This means that after Friday, there may be a certain “anti”-gravity around those spots until gamma is refilled.

Ok fine, massive expiration and trillions in gamma rolling over. So what? Doesn’t the Fed’s hawkish shock take precedence?

Well, no, because as Nomura’s Charlie McElligott warns in his letter today, people are confusing correlation with causation here: “Equities stable on hawkish Fed guidance” is the wrong read here, as per the “2013 Taper Tantrum,” the “Yellen 2015 Liftoff” and “Powell 2018 QT” backtests—instead, equities are stable for the same reason they’ve been chopping for weeks: markets continue choking on an oversupply of Gamma from Vol sellers, a trend which will peak tomorrow and is set to reverse as trillions in gamma exposure have to be reloaded.

This is why, McElligott writes, he has been pounding the table on this particularly enormous Quarterly Op-Ex print, “because we’re in the process of working-through a precipitous drop in both $Gamma and $Delta around this serial “quad witch” expiration, which in-isolation should leaves us susceptible to a much wider trading-distribution coming-out.”

Translation: enjoy today’s melt up because tomorrow it’s about to hit the fan.

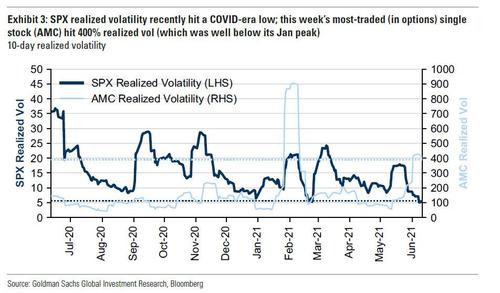

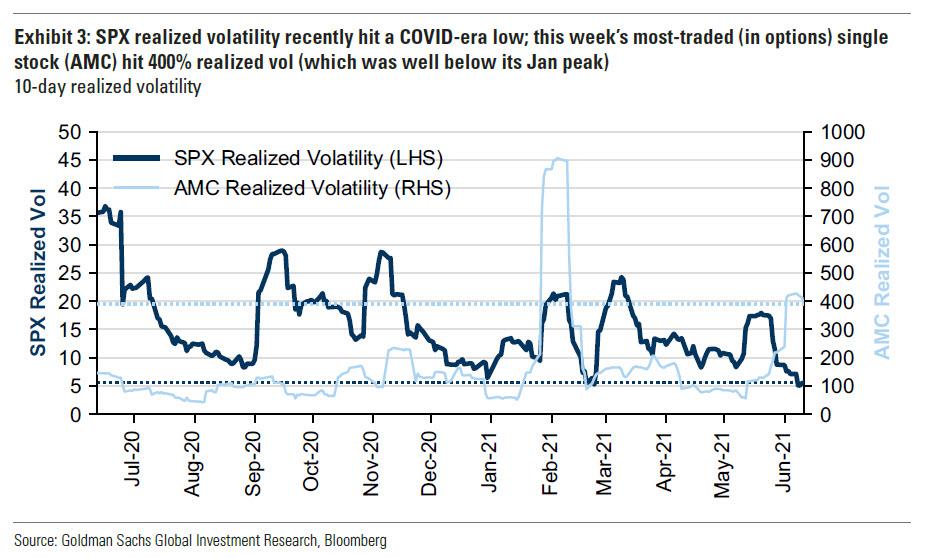

It’s not just Nomura that is warning the market can crack after tomorrow’s quad-witch: as a reminder, Goldman’s derivatives strategist Rocky Fishman wrote earlier this week that the extremely low recent SPX realized volatility…

… “is consistent with the possibility that 18-Jun has left “the street” long index gamma,” in which case Fishman echoes what we also said last week, namely that “realized volatility could pick up once positions are cleaner.”

Meanwhile, the rising beta of VIX futures to the SPX indicates that investors expect short gamma dynamics to pick up should markets sell off.

Translation: the market will become much more volatile in a selloff.

How much more volatile? According to an update from McElligott, a massive ~35% of SPX options Gamma towill drop-off tomorrow, 52% of QQQ, 61% of IWM and 54% of EEM. These are staggering numbers and explains why we are having a market-wide gamma meltup, which however is set to end with a bang tomorrow when it all reverses. McElligott explains as much:

Despite so much of the overall Gamma and Delta rolling-off, the poster-child in this latest iteration of the Equities “Short Vol” movement—the “Gamma Hammer”—was back both before-and-after the Fed and selling even more short-dated SPX strangles, which in-turn, back-filled the Street with more “Gamma” and created Equities to BUY into any pullback—the self-fulfilling prophecy rinses & repeats…

With that stabilizing and seemingly never-ending Dealer “long Gamma” insulation created from various Vol Sellers, we continue having a hard-time holding, let alone extending, any selloffs—particularly as the market still believes that if this “hawkish messaging” were to spill over into a larger pullback in risk-assets (hint: stocks) and an extended and prolonged tightening of US financial conditions—that the Fed will yet-again “bend the knee” to markets.

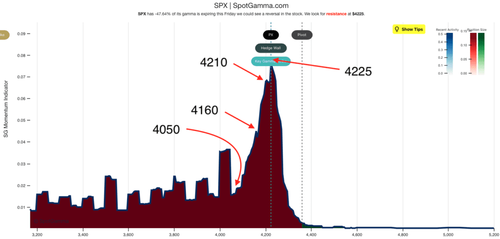

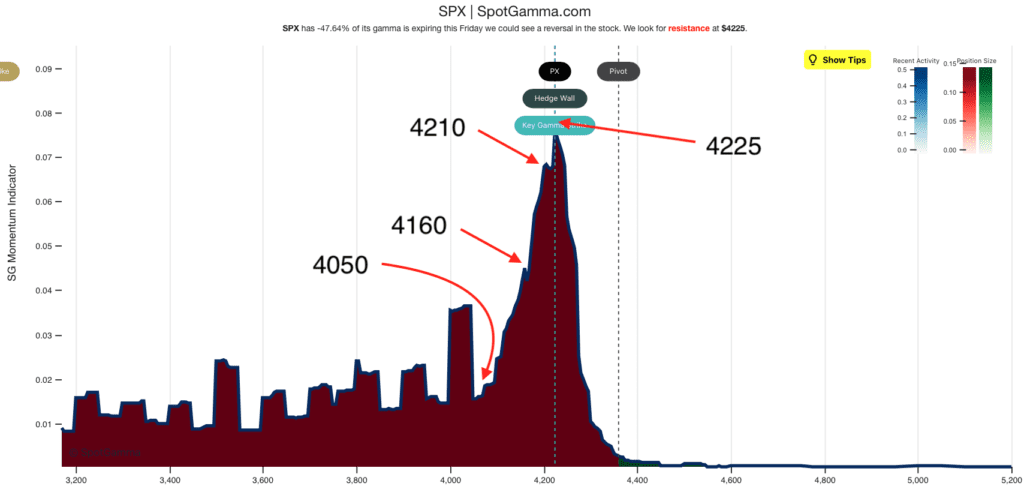

Yet while massive gamma selling explains today’s meltup, tomorrow it’s an entire different ballgame, and as our friends at spotgamma note, once most of the gamma gravity is gone (when it expires tomorrow), the gamma goes into reverse, and as SpotGamma’s EquityHub view shows, we are looking a substantial downside risks:

Sharp changes in the SG Momentum Index (Y axis) infer volatility, and you can see that we show 4160 as first support (based on that “node” as marked) and then 4050 area would be a reasonable stopping point given the massive amount of open interest that picks up into 4000.

As SpotGamma ominously concludes, “there are times wherein we mark risks as quite high, and we see this as one of them. This, of course, does not mean that markets decline sharply but our models see that as a distinct possibility and so we are lending a bit more focus to that “tail” in this note.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}