The following is a guest post from Doug Pless.

As I have discussed in previous articles, I begin my morning preparation by reading the SpotGamma AM Report when I plan to trade futures. For ES futures, I note gamma levels and key metrics for SPX and SPY. For NQ futures, I note Gamma Notional, and the Volatility Trigger, Put Wall, and Call Wall gamma levels for QQQ.

When I plan to trade NQ futures during the day, I also look up QQQ in Equity Hub. First, I review the data and note the Hedge Wall and Key Gamma Strike. The Hedge Wall is the strike where the largest change in gamma is detected. The Key Gamma Strike is a strike where volatility may increase or decrease. Both levels can act as pivot or pin areas.

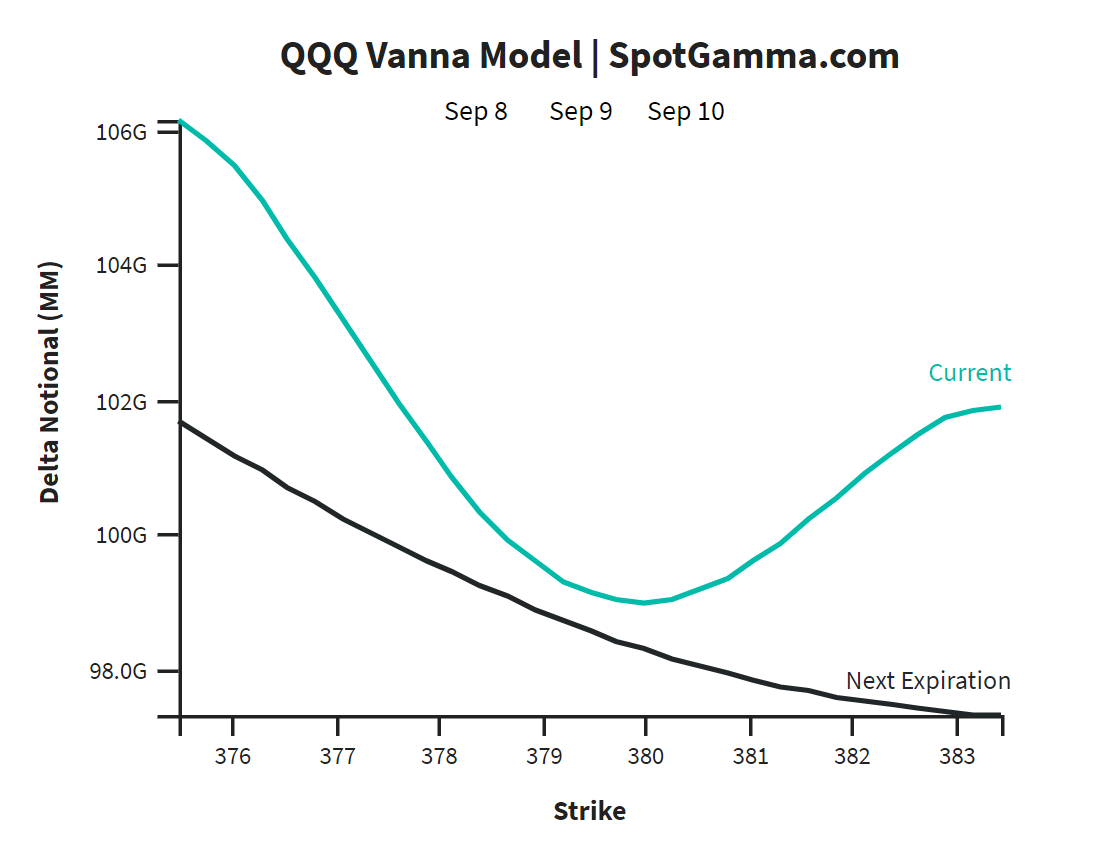

I also look at the Vanna Model for QQQ. This graph shows how market maker delta exposure may shift as price and implied volatility (IV) move up or down. The slope of the lines indicates how aggressively market makers may have to buy or sell NQ futures to hedge their delta exposure as price and IV change.

Finally, I watch the HIRO Indicator in the first minutes of trade after the RTH open. The HIRO Indicator shows the market maker hedging impact of options trades. Market maker hedging flow can have a significant impact on order flow in NQ and is often a good confirmation of price direction.

Based on this information, I develop a thesis regarding anticipated volatility, trading range, and directional bias for the day. An example of how I used this information to plan and execute a trade is shown below.

Trade Example #1: September 10, 2021

On September 10, the following metrics for QQQ were shown in the AM Report and Equity Hub:

- Gamma Notional: -$509 MM

- Volatility Trigger: 381

- Put Wall: 378

- Call Wall: 390

- Hedge Wall: 380

- Key Gamma Strike: 380

The QQQ Vanna Model for September 10 showed a significant downside skew indicating market makers would need to aggressively sell NQ futures to hedge their delta exposure as price moved down. The QQQ Vanna Model for September 10 is shown below.

Based on the negative Gamma Notional and skewed Vanna Model, I was looking for a higher volatility day with a wider trading range. Market makers would likely be trading with the directional movement of the market rather than against it.

A few minutes after the cash open, price began to move lower and market maker hedging flow shifted from bullish to bearish, as shown by the HIRO Indicator in the Bookmap chart below. The indicator showed that market makers were selling NQ futures to hedge bearish option trades in QQQ as price moved down, confirming the Vanna Model. Based on the Vanna Model and HIRO, I was looking for opportunities to join the move. There were several short setups in the morning as price moved toward the QQQ 380 Key Gamma Strike (shown in the second image) and the Combo L3 level below.

The final image below shows how the day played out. NQ price action and market maker hedging flow were in line with the QQQ Vanna Model, which showed that market makers would need to sell NQ futures to hedge their delta exposure as QQQ moved lower toward 376.

For further definitions and information on the terms used in this article, please see the SpotGamma Support Center for a list of dozens of SpotGamma proprietary terms, as well as context for common market terminology.

SpotGamma Products Used:

- SpotGamma Pro

- HIRO Indicator (available now on Bookmap)