Here is a strategic way to look at options trades into earnings.

1) Estimated Earning Move and Implied Move

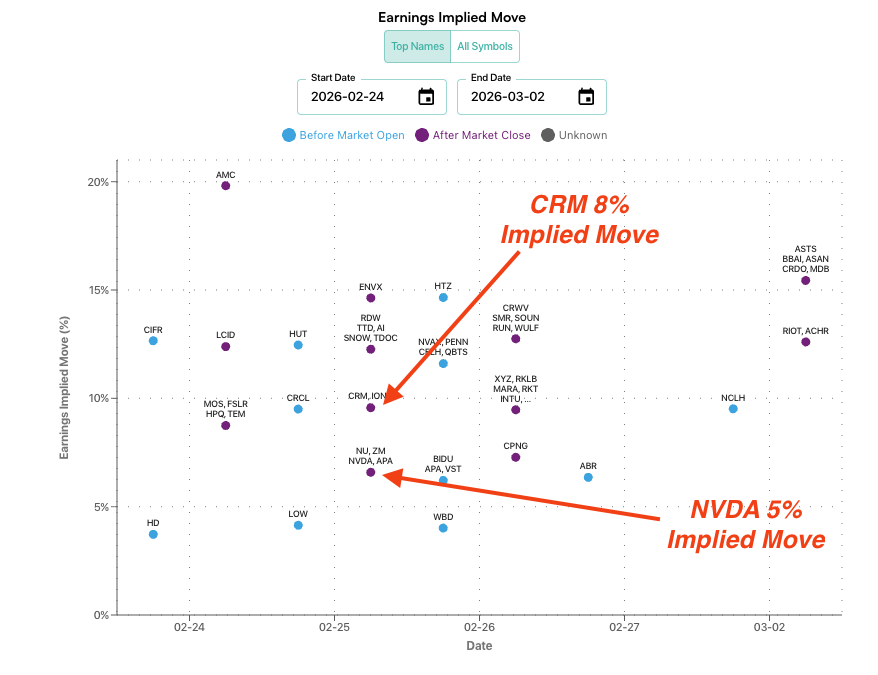

You can use our free earnings implied move plot to do this. Here we see CRM has an 8% implied move for earnings, and NVDA has a 5% implied move for earnings. Both report on 2/25/26.

2) Evaluate How Cheap or Rich Options Are

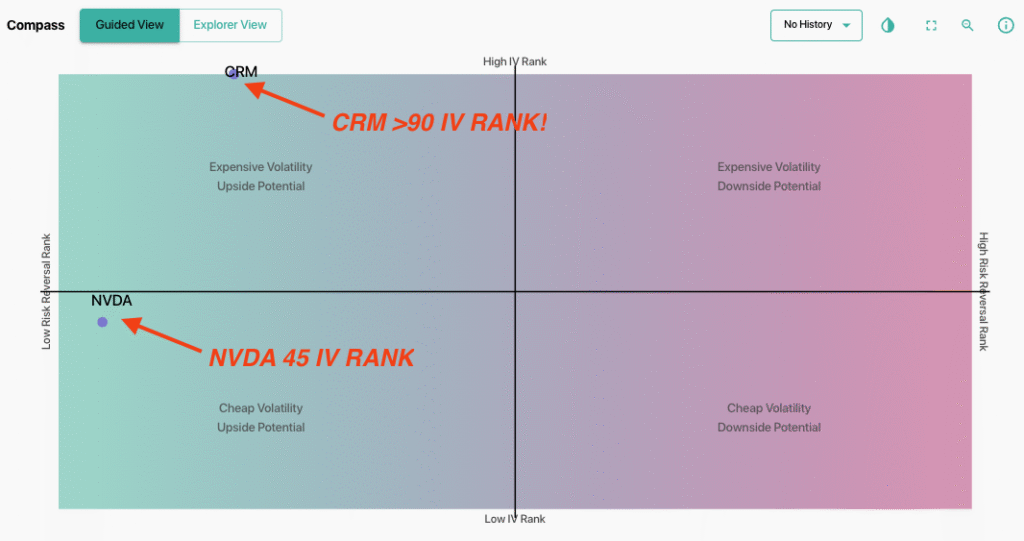

Compass, below, plots how 1-month options prices are marked relative to the last year of data.

For both stocks we see the plot points are on the left of the grid, which tells us puts are rich relative to puts.

Second, we see the IV Rank is +90 which tells us that options are now more expensive then they have been in the last year. Remember, the April tariff market implosion was within the last year!

NVDA, at a rank of 45, is pretty typical for a stock about to enter earnings. Given this, CRM seems like it has way more volatility premium.

3) Estimate the Potential Change in Options Volatility

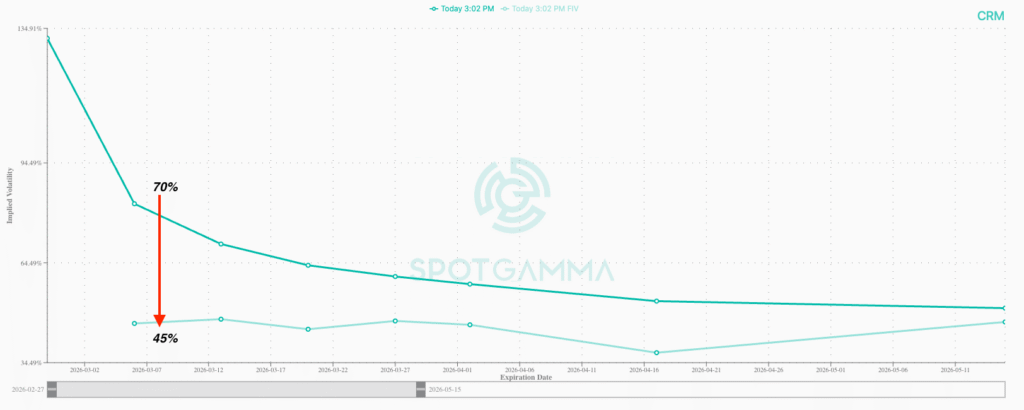

Here we have 1-month skew for CRM (dark teal). The skew is in backwardation, due to the volatility of the stock and sector, as well as earnings.

The lighter teal line is our forward implied vol, which is a metric used to determine where volatility may move after an event. Based on this metric, we think that 3/6/26 expiration IV may decline from ~70% to ~45% – that is a massive 25 pt vol decline.

4) Estimate Potential Options Trade Profit and Loss

SpotGamma has an incredible options calculator that allows you to project trade PNL’s in many unique ways.

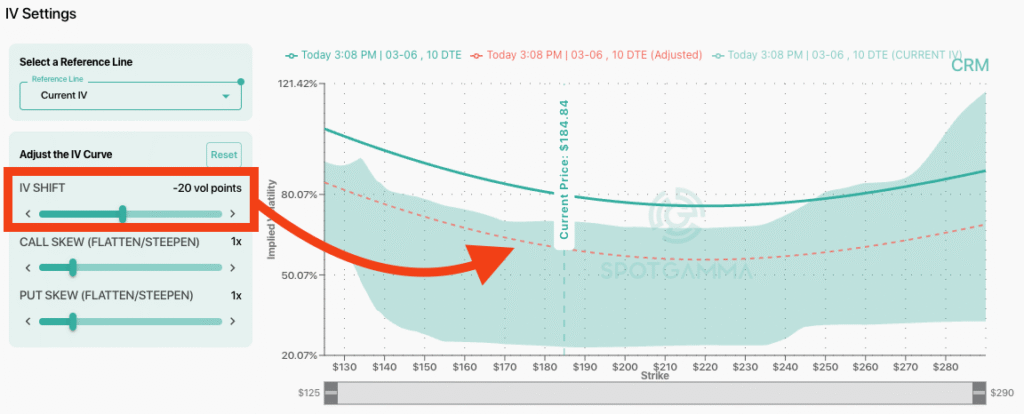

First, we load up the 3/6/26 expiration straddle, which is a way to trade a stocks volatility for about $19.25 We then click on the “IV Settings” button so that we can customize vols.

We adjust the IV by 20 vol points, leaving some room relative the full 25 vol point contraction noted above. As you can see, that shifts the skew down from the current level (teal line) to a new level (red dashed line).

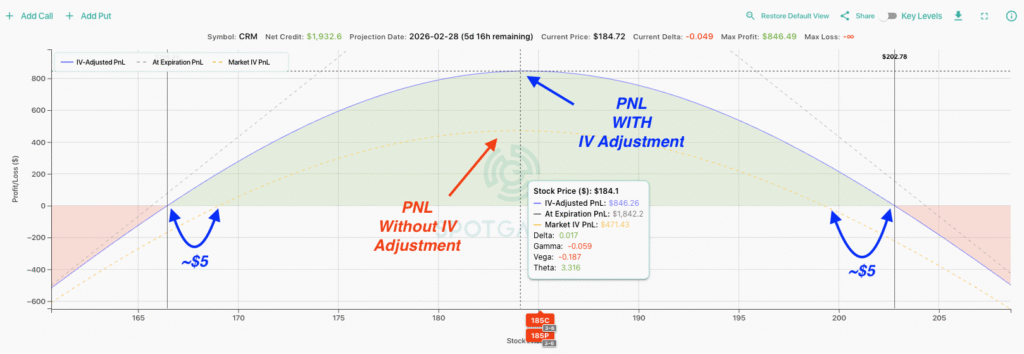

This new projection now shows up in the PNL plot. The stock price is on the X axis, and the PNL is on the Y axis.

What the PNL plot depicts is the PNL of the short straddle if you use the current IV (dashed yellow) vs our new IV (blue). What you can see is that if earnings does drop implied vol, the PNL from a short straddle trade increases from an estimated $470 to $845 – that is 80% higher if our IV decline is correct.

Further, the break even PNL improves by $5 on each wing – meaning, the stock has to move $5 further in order to shift our PNL to a negative position. This shifts the estimated breakeven to $167 from ~170, and on the upside to ~202 from ~199.

That is an extra 1-2%, which equates to about $3-4 in the stock.

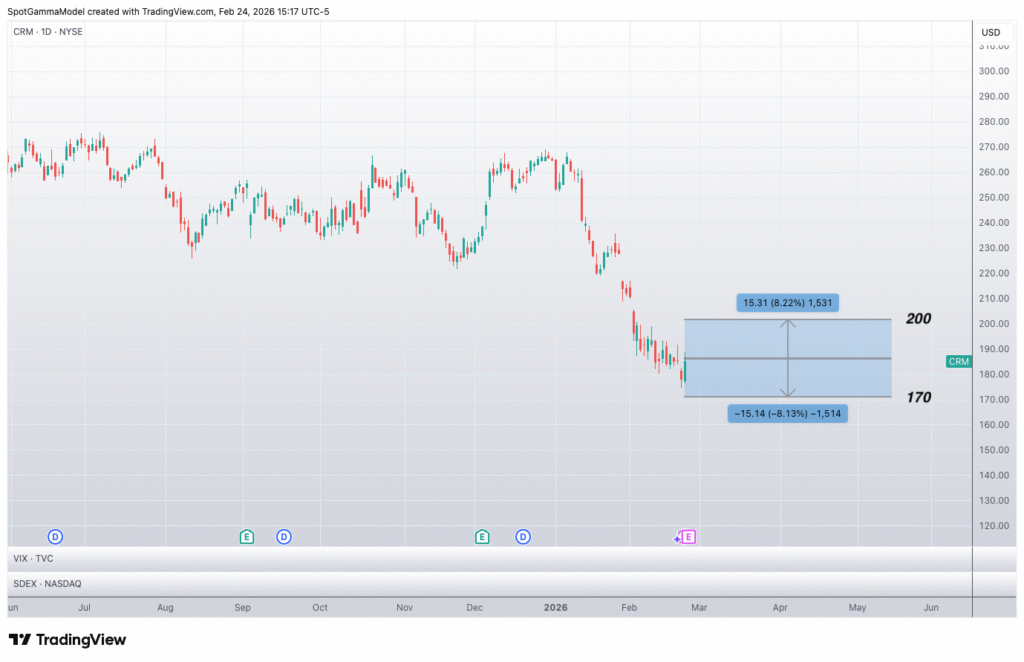

Thinking back to the CRM implied move of 8%, and assuming the stock is at $185, traders are pricing in CRM stock to stay between $200 and $170 after earnings.

Our argument here is that the straddle, or other short options structures may have a much better opportunity to profit when the IV is excessively high.