The S&P 500 delivered a volatile week: Tuesday began with risk-off positioning and a negative gamma environment, evolving into Thursday’s explosive rally, finally culminating in Friday’s blowoff top.

The result? SPX closed almost exactly where it started the week at 6,482.

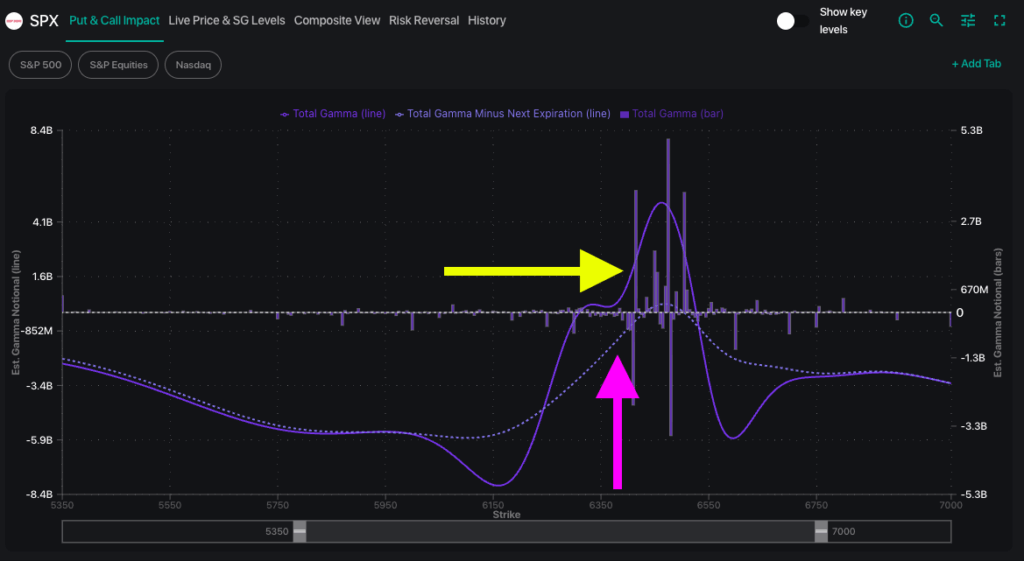

By Wednesday, 0DTE options hit a record-setting 70% of all options volume, keeping the market in check through largely positive gamma. Beyond these short-dated flows however, dealer positioning actually remains largely negative, particularly below SPX 6,400 and above 6,525.

This past week began a new chapter in 0DTE options dynamics: Captain Condor’s 50,000 contract position vs. the systematic “Seek-and-Destroy” algo trade.

The Seek-and-Destroy algo has recently emerged as an end-of-day phenomenon that has driven SPX towards specific strikes through repeat option-buying until a price target is achieved.

Each day this past week, this algo trade targeted legs of the Captain Condor position through consistent call buying that forced massive upward delta hedging from market makers, effectively neutralizing gamma at Captain Condor’s chosen strikes by weaponizing billions of dollars in extremely short-dated flow.

This 0DTE occurrence is now something all traders should pay attention to: given the prevalence of short-dated flows, these positions now drive meaningful price action across the entire S&P 500 complex.

The VIX Setup: Growing Precarious

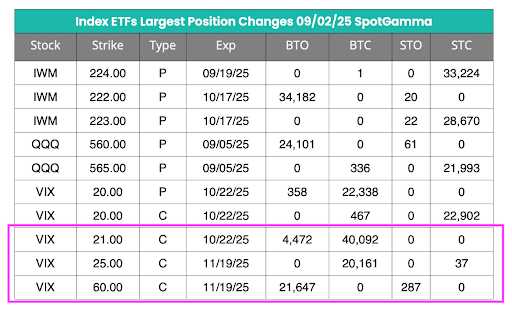

One of the most important positioning developments seemed to fly under the radar this week: the build-up of VIX call positions, as detected in our daily FlowPatrol™ report.

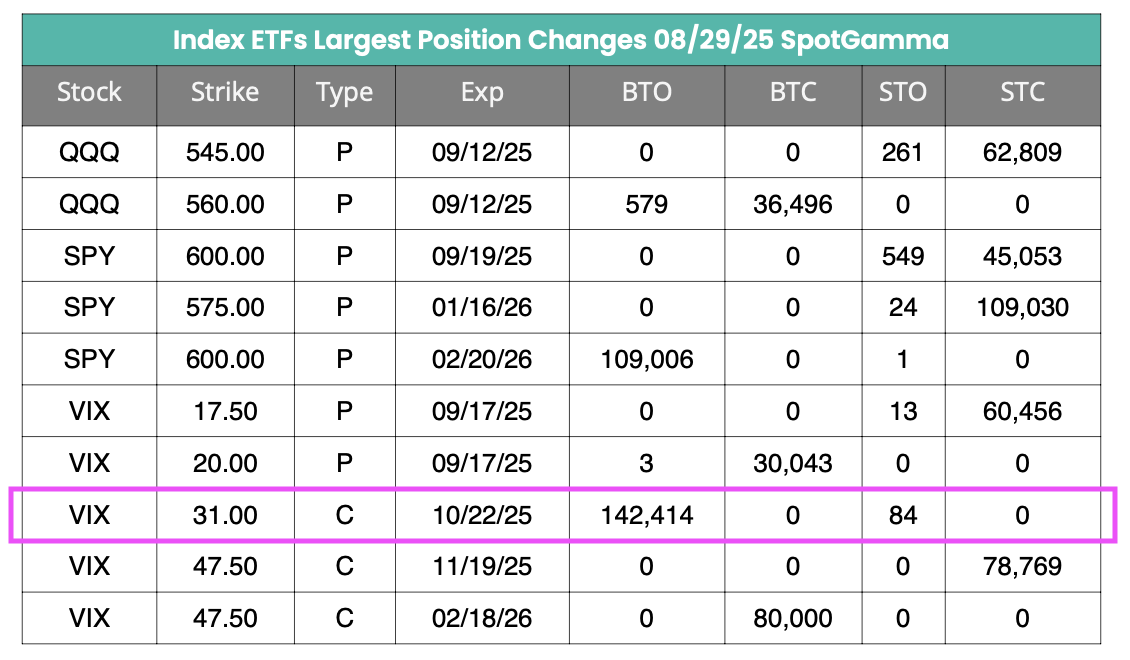

With 40k VIX October 21 calls added early in the week, following a massive 142k VIX 31 call position bought last Friday, institutional buyers appear to be setting up for potential volatility expansion.

Why does this matter? Large VIX call positioning has created a dealer hedging dynamic that can amplify price movement in either direction. A vol spike could trigger forced VIX buying that cascades into equity selloffs, while sustained low volatility could force aggressive covering and drive sharp rallies.

Looking Ahead: Software Earnings and September OPEX

Next week’s key earnings include Oracle (ORCL) reporting before market open on 9/9 with a 8% implied move, Rubrik (RBRK) after close on 9/9 with the highest volatility expectation at 15%, and Adobe (ADBE) after close on 9/11 with a 8% implied move.

From a macro perspective, Wednesday’s PPI and Thursday’s CPI readings will help define expectations for the September 17th FOMC meeting. These data points could significantly influence Fed policy expectations and market positioning heading into the decision.

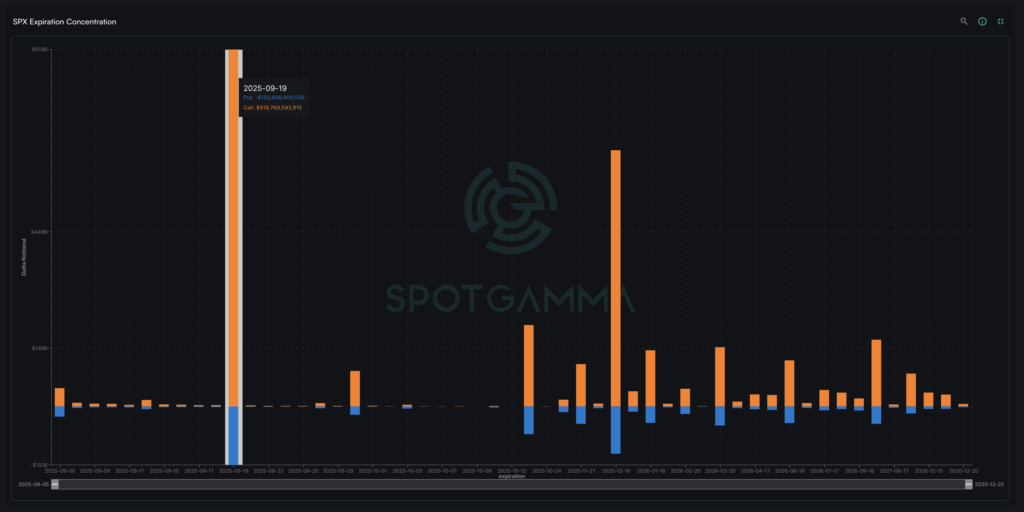

Adding another layer of complexity, September OPEX represents one of the largest expirations ever, with more than $700 billion in delta notional expiring.

This triple-witching expiration will likely reduce the current stabilizing influence of dealer positioning, with the potential to shift the broader market out of its long gamma environment. We watch for amplified volatility on and after September 19th as major positions expire.