SPX ended the week at a major SpotGamma support level of 6,450, driven by a combination of volatility compression, stabilizing dealer hedging flows, and the power of large options positioning.

This week followed the trajectory outlined in our Founder’s Note on Monday morning: a benign CPI reading sent volatility even lower, and the SPX rose from 6,360 to a peak of 6,481 before the hot PPI tamed the exuberance. Record-low implied volatility throughout the week meant that traders were only pricing in mild corrections at most from any given event — facilitating a steady grind upwards.

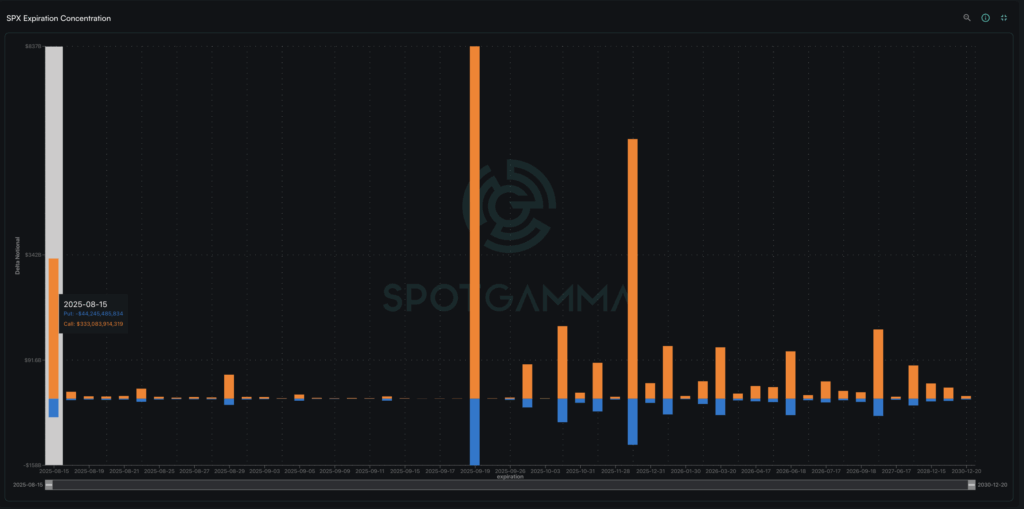

OPEX served as one of last week’s catalysts to watch, and Friday’s expiration featured over $370 billion delta notional exposure rolling off, the largest expiration until September 19. As expected, the call-heavy positive gamma environment (88.7% of SPX delta were from calls) created natural resistance around 6,500.

While equities celebrated, rally-driving sectors such as crypto began flashing warning signs. ETHA – an Ethereum ETF – hit 100% IV rank by Monday’s close, and our analysis flagged this as a potential short-term top. Sure enough, crypto ETFs were under heavy selling pressure by Friday.

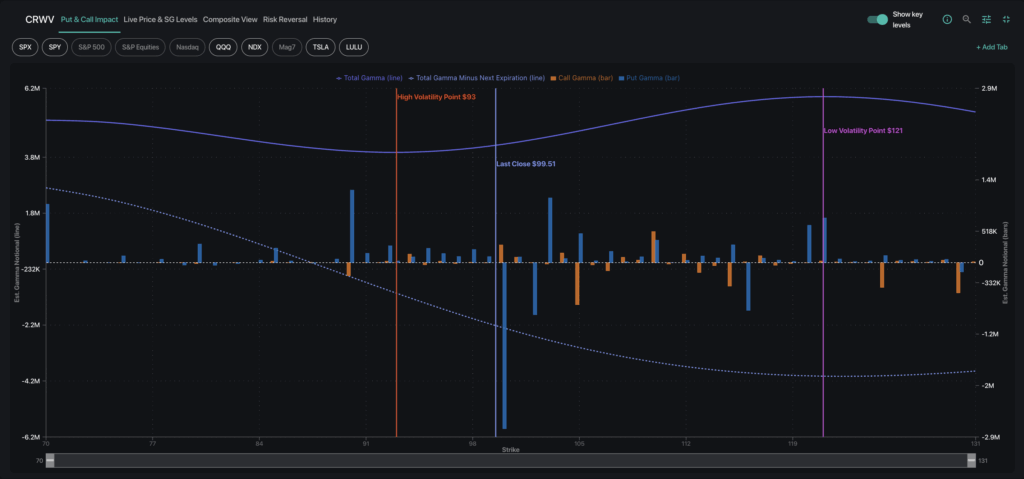

Trade Highlight: CoreWeave’s Sharp Drop

CRWV experienced a bloodbath after earnings and lockup expiring this week, plummeting 36% from $150 to the $95 area. Although price somewhat stabilized in a sticky positive gamma zone near $100 level, CoreWeave’s options positioning shifts markedly more negative after Friday’s OPEX (lower line on the chart below).

After Friday’s expiration, CRWV now sits in a precarious zone between stabilizing support below, and negative gamma above where we would anticipate elevated volatility and amplified moves in either direction.

Jackson Hole Is Now the Wildcard

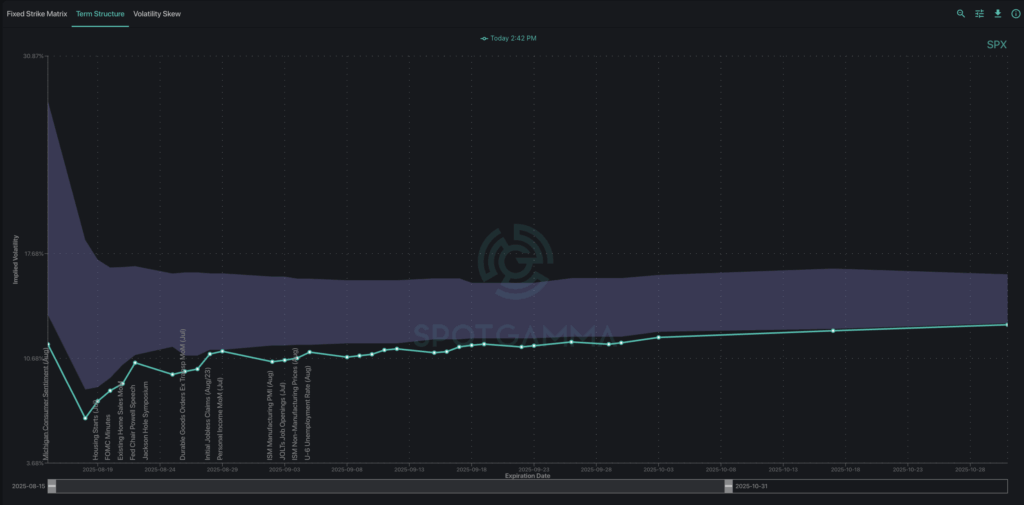

Here is what concerns us: volatility is at record-lows across major indices and most other asset classes. SPX IVs for the next 10 days are sub-10%, and rate cut expectations remain unchanged despite Wednesday’s hot PPI. When consensus becomes this extreme, fragility builds beneath the surface.

Three catalysts could shatter this calm:

- VIX expiration (8/20) often provides the spark for positioning resets

- Jackson Hole (8/22) where Powell’s tone on rate cuts will be scrutinized

- NVIDIA earnings (8/27) with the stock now representing 8% of the S&P 500 — allegedly the largest single weight ever

Of the 3 events, the Jackson Hole Symposium represents the largest market-wide vol catalyst. With rate cut expectations now at 90%, any hawkish surprises could trigger the type of volatility spasm that caught markets off-guard on July 31st.

Our term structure analysis reveals IVs are still priced for perfection. This creates asymmetric risk: limited upside if Powell stays dovish, but significant downside if he hints at a more measured approach to cuts.

Our positioning strategy remains defensive yet opportunistic. September VIX calls and end-of-August SPX put spreads may be attractive — not because of any underlying bearish signals, but because volatility is simply too cheap to ignore.

As we noted in Thursday’s pre-market Founder’s Note, “The money to be made betting on the fully priced-in outcome is essentially zero.”

This could mean we’re in the calm before the storm, like a rubber band that gets stretched too far: when it snaps, it can be hard and fast.

Track these unfolding dynamics with SpotGamma’s suite of options analytics, including special positioning insights in our new daily FlowPatrol report.