The following is a guest post courtesy of Michael Kramer of Mott Capital Management.

Jay Powell will speak at next week’s Jackson Hole Economic Symposium. Some investors think it may be where he lays out the Fed’s path towards the tapering of asset purchases. Recent economic data suggests that inflation is running at levels that meet the Fed’s 2% average.

In contrast, the current employment data has shown substantial job gains over the past two months.

The only question is if this data is enough to indicate that significant further progress has been achieved and if it warrants the removal of the ultra dovish monetary policy the Fed instituted as a response to the pandemic.

The markets seem to be preparing to remove some of the accommodative conditions in the months ahead, based on the recent strength in the dollar and rising short-term rates. Additionally, the yield curve has flattened, suggesting that the market expects the removal of these easy conditions to slow future economic growth.

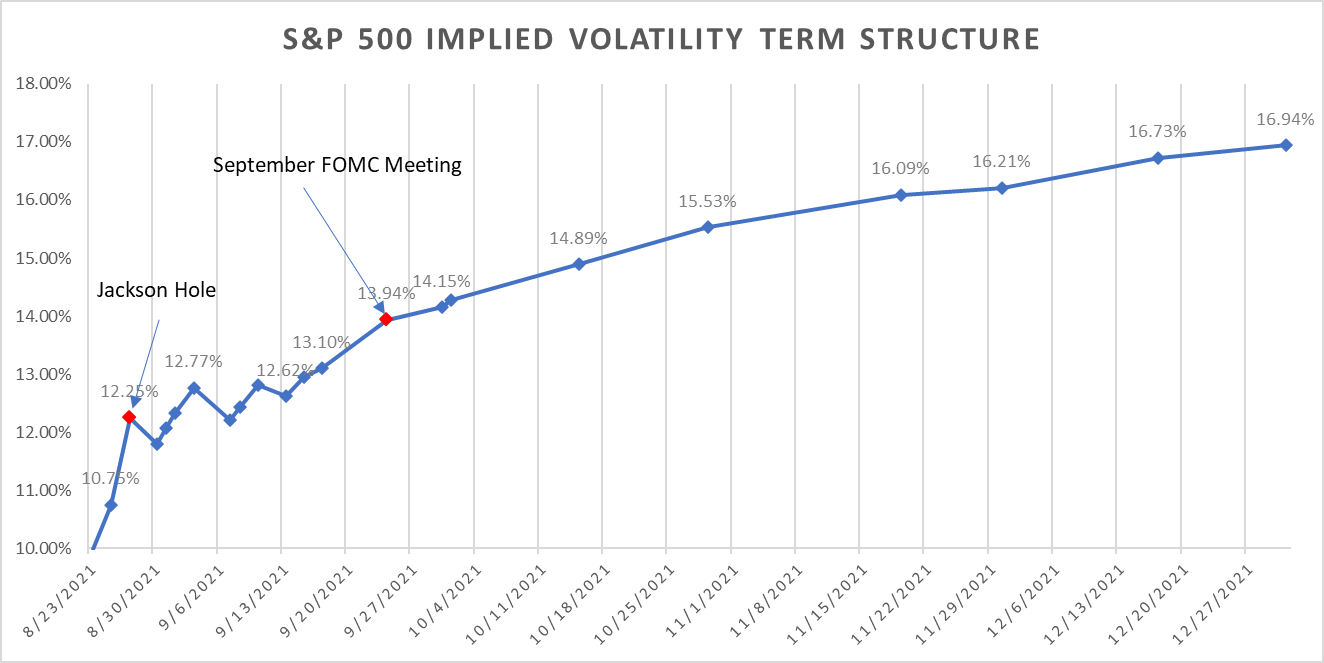

S&P 500 Options Suggest Increased Volatility Around The End of September

It isn’t just the bond and currency markets preparing because the equity market appears to be getting the jitters, too, even though one would never know it based on the S&P 500, which seems to set a new record on what feels like a daily basis.

But the nervousness is there and is especially seen when looking at the implied volatility term structure of the S&P 500, which shows a bump in implied volatility levels on August 27, rising to 12.25% versus the 10.75% for August 25. That curve grows steeper when moving out to September 24 around the next Fed meeting, which is on September 22, climbing to almost 14%.

Additionally, the open interest for the S&P 500 options supports the idea that the market is especially concerned around this end of September timeframe. The open interest levels for the S&P 500 options are the greatest for the expiration date on September 17. Meanwhile, the September 30 weekly expiration date carries a more substantial open interest than the November monthly expiration date.

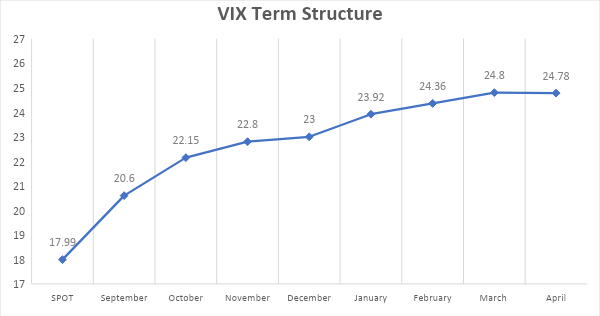

The VIX Suggest Volatility Is To Rise Into Year-End

The VIX term structure also reflects the same type of risks being built into the market. However, what is even more noticeable is a bump that takes place from December to January. This jump in the VIX might suggest the market is pricing in additional risk around the beginning of the year. Perhaps there is a belief that a taper will be announced formally around the September FOMC meeting, with the actual process starting sometime in January.

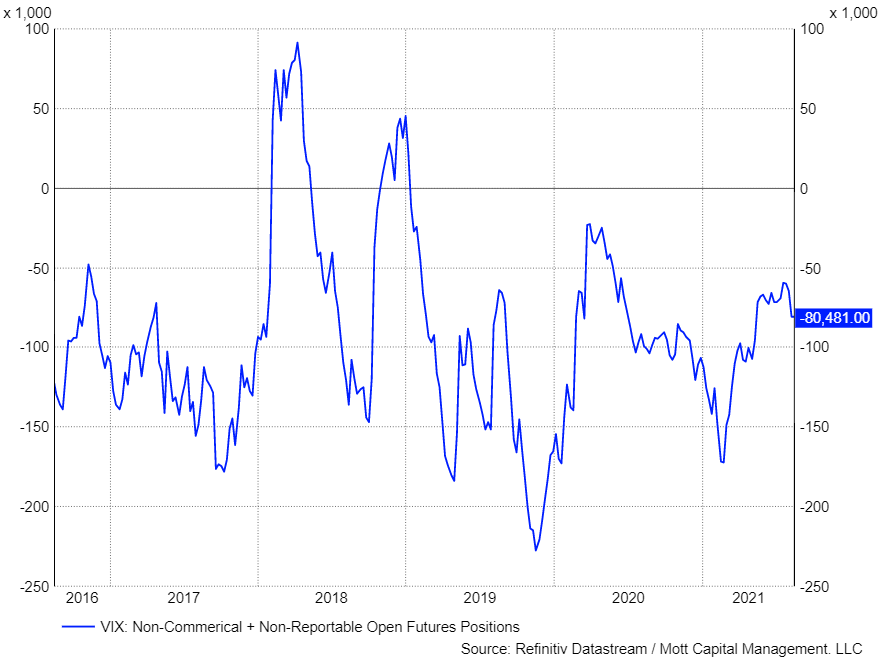

Additionally, it seems that the speculators in the futures market have been reducing the amount of VIX futures contracts they are net short. The number of net short contracts has risen sharply since February and took another leg higher at the beginning of May. This is after months of building a substantial net short position starting in March of 2020.

The recent reduction in this positioning could be an indication that speculators overall are beginning to ease up on shorting the VIX at these lower levels and not believing there is much more downside. It could also suggest that these same speculators are worried about a potential move higher in the value of the VIX in the months to come.

It seems that the market is preparing for a significant change to occur in policy, and it would seem the timing of that change could happen very soon. In the end, it may not matter when the Fed officially flips from easy monetary policy to tightening monetary policy, but that it will.

The market appears to be pricing in additional risks from every angle you can look at it.