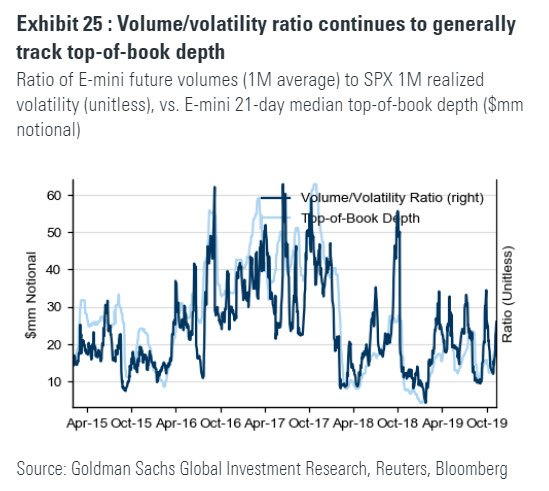

As volatility spikes S&P E-mini top of book depth decreases. Anecdotally this doesn’t come as a surprise because higher volatility should make dealers reduce size and be less aggressive. Whats interesting is that (in theory) in a negative gamma world options hedgers don’t reduce their size, so they just face less liquidity which means their hedging has a larger impact in markets. This lack of liquidity may be the reason we see such bigger volatility when gamma is negative versus positive.

You could use a model like ours or Nomuras to estimate that impact. If notional gamma is, say $25 billion per percent move in the S&P500, then dealers would hypothetically have to trade ~155,000 futures ( $25bn/(SPXPX * $50)). Not all that volume would be done in one chunk, and there are several caveats to that figure but for it illustrates the potential impact.