The following is a guest post courtesy of Michael Kramer of Mott Capital Management.

The S&P 500 has fallen by more than 10% in the past two weeks, and to say that it is due for a bounce may be an understatement. The combination of a 75 bps Fed rate hike and massive June quarterly options expiration resulted in the S&P 500 posting back-to-back weeks with drops of more than 5%. Don’t be surprised if we get a snapback rally, even if it is only a short-term bounce.

Stocks Are Due To Rally

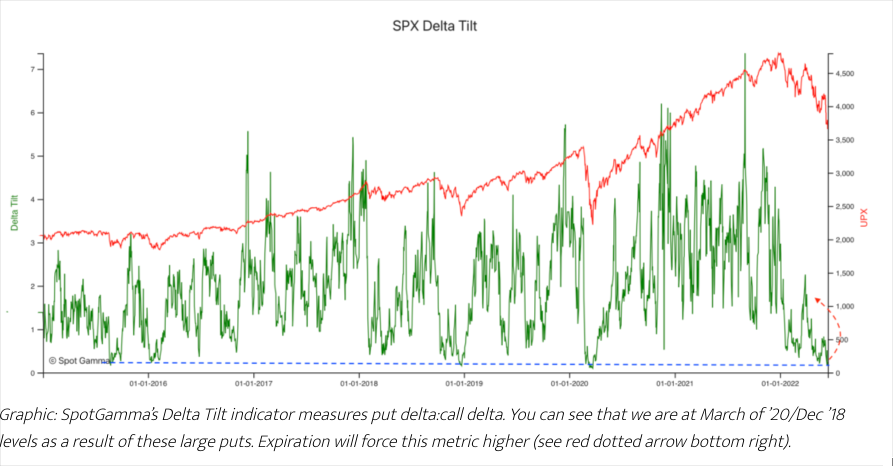

The SpotGamma Founder’s notes have shown that markets may be stretched to the downside, based on the S&P 500 Delta tilt, now at levels equal to December 2018 and March 2020. While the stock market can see a rebound from these oversold conditions, a big, sustained rally is not as likely, given that the Fed is raising rates and reducing its balance sheet versus a Fed looking to ease monetary policy in late 2018 and early 2020.

Also, since the beginning of the year, there have been six options expiration dates. In four of the previous five expirations, the S&P 500 rebounded from its pre-option expiration sell-off or consolidated sideways. The only time there wasn’t a countertrend rally was in March, which saw the S&P 500 rise sharply into options expiration and rally following the expiration date.

On top of the options cycle, a significant risk was removed from the market this week, with the Fed raising rates by 75 bps. The next Fed meeting is not until the end of July, which clears a path for a period of calm until the next big Fed event, which will come when the minutes for the June FOMC meeting are released around the first week of July.

Since the beginning of the year, there have been 4 Fed meetings, and while we do not know the path the market will take following this latest June meeting, we do know that during the prior three FOMC meetings, the market rallied twice and consolidated sideways once. Additionally, the Fed minutes have been released four times, and all four times saw the markets lower by the time of the FOMC meeting.

I wrote about this phenomenon in April, discussing the notion of, “Buy the Fed meeting. Sell the Fed minutes.”

Mechanical Reason To See A Bounce

From a mechanical standpoint, there may be a good reason for these two market patterns in 2022. The Fed meeting presents an event risk, which causes traders and investors to look to hedge their portfolios. This increased hedging activity creates more put option buyers and increases implied volatility levels. This action causes options dealers to short S&P 500 futures, pushing markets down. Meanwhile, once the FOMC meeting ends, there is a process of de-risking that drives implied volatility levels lower, causing puts to lose value and options dealers to reduce short positions. On top of this, option expiration helps reduce gamma levels, meaning option dealers have lower levels of hedging that need to be maintained, providing less of a headwind for markets to move higher.

A Rally May Not Last Long

It is important to note that the risks for declines remain very high, especially given that the Fed is likely to continue hiking interest rates which will weigh heavily on equity markets. This is the opposite of the December 2018 and March 2020 experiences, which saw the FOMC easing monetary policy. Additionally, with options expiration now past, as pointed out in the SpotGamma Founder’s note, the risk for traders and investors to establish new put positions means option dealers will be forced to hedge negative deltas and potentially help push the S&P 500 lower.

While a countertrend rally could certainly be long overdue, it isn’t likely to last very long, as significant risks are likely to build again heading into the next Fed meeting and options expiration cycle.