The S&P 500 spent early July grinding higher with sector rotation quietly forming beneath a calm index. As SPX price action remained relatively muted over the past week, implied volatility dropped to near-record lows as of Friday: IV for contracts expiring next week now sit in the 6-10% range.

Regardless of any directional bias for this market, positioning for a volatility spike has rarely been cheaper.

The backdrop heading into this week has been one of rotation rather than direction. July so far has seen capital shift between sectors while index-level volatility expectations have remained subdued. In short, individual stocks and sectors moved meaningfully, but those moves largely offset one another at the index level.

What could make conditions ripen for an uptick in volatility — and a spike in options prices? We see three likely catalysts: a dense macro calendar, the start of earnings season, and July OPEX all land within a five-day window.

Looking at the volatility landscape, the low demand for protective puts stands out to us in particular. Even with significant positive gamma set to roll off after July OPEX — an event that typically leaves the market with less built-in stability — hedging activity in SPX index options remains muted. Traders do not appear to be reaching for downside protection, and that lack of demand is helping keep implied volatility historically depressed.

Cheap Options, Loaded Calendar

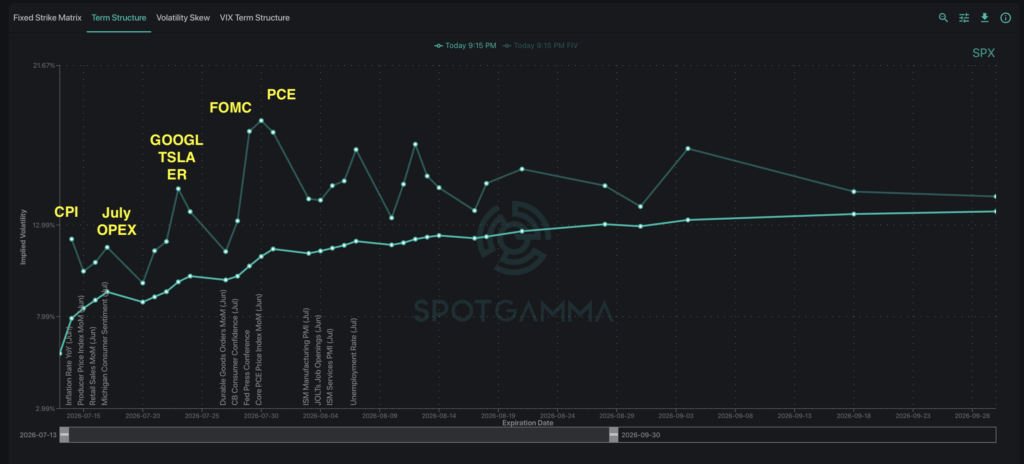

The pricing of volatility tells a story of complacency. One-month realized volatility is running near 15%, while the current at-the-money implied volatility term structure sits closer to 10%. When options are pricing in less movement than the market has recently delivered, they appear relatively inexpensive.

Additionally, forward implied volatility currently rests above the at-the-money Term Structure for key upcoming events. This suggests that potential risks may not be fully priced-in.

The forward-IV gap matters because next week’s calendar is packed: CPI on July 15, PPI on July 16, Retail Sales on July 17, and July OPEX on July 18.

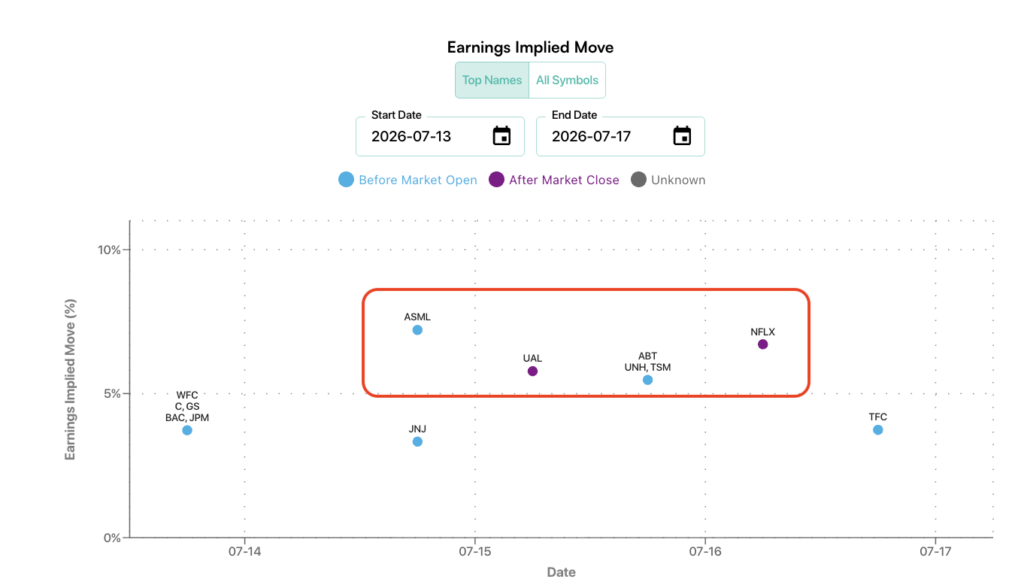

In addition, the market will digest earnings from the major banks (JPM, BAC, GS, WFC, C, MS), healthcare names (JNJ, UNH, ISRG), and big tech companies (ASML and Netflix) — all in the same week.

For those trading the S&P 500, put flies in SPX or SPY may appear attractive, as we discussed in our previous Founder’s Note. These structures are currently inexpensive hedges for equity portfolios given the low IV, should realized volatility pick up meaningfully from a catalyst-heavy week ahead.

NFLX Earnings Presents Trade Opportunities

Earnings season presents unique trading opportunities — alongside the risk that accompanies each earnings event. Our session last week on Trading Earnings explained these dynamics featuring several relevant examples.

From the upcoming earnings calendar, ASML and NFLX currently carry quite large options-implied moves at roughly ±7%. NFLX in particular, presents an interesting setup heading into earnings, with positive dealer gamma below the current price and negative dealer gamma above it.

Using our Synthetic OI model, we can observe approximately ~100k lots of puts sold by traders at the 65 strike for NFLX. That positioning creates a likely support area near 65, which also aligns with the lower bound of the options-implied range.

To the upside, gamma flips near 75, where dealer positioning transitions from positive to negative gamma. If Netflix were to break above this level, the move could accelerate quickly as negative dealer gamma amplifies directional price movement. Netflix closed just above 73 on Friday, after declining roughly 28% over the past three months.

For traders looking to express a bullish view, we see two structures worth considering:

- Selling put structures (with appropriate protection) near the 65 level to harvest elevated single-stock implied volatility

- Deploying defined-risk 80/100 call spreads expiring after earnings to position for continued upside.

Note that the above discussion strictly reflects our analysis of options positioning, and is not an investment recommendation or advice.

We’ll be tracking positioning changes as we see them, with an eye towards the macro calendar, earnings season kicking off, and July OPEX. With the monthly expiration removing a meaningful portion of the market’s stabilizing gamma at week’s end, we must wait and see how options positioning resets for the second half of July.