Markets pushed to fresh all-time highs this week, driven by continued strength in AI stocks. One of the notable stores was SMH (the semiconductor ETF) which surged over 30% this month to cap 168% gain in the past year.

While euphoric spirits have recently prevailed, next week brings an event-heavy calendar that might shift the options landscape considerably.

Five Mag7 companies report earnings: Amazon, Microsoft, Apple, Meta, and Alphabet. Qualcomm reports as well, and the Federal Reserve’s rate decision lands on top of that earnings stack. That concentration of catalysts in a single week is rare — and sets the stage for event-driven movement that traders can position around.

Why Volatility May Be Underpriced Into Next Week

With a packed line-up of events next week, it’s important to monitor implied volatility to understand how traders are positioned across the market. In last week’s newsletter, we flagged a notable setup: index implied volatility remains below realized volatility — meaning options have been pricing in less turbulence than markets have delivered recently.

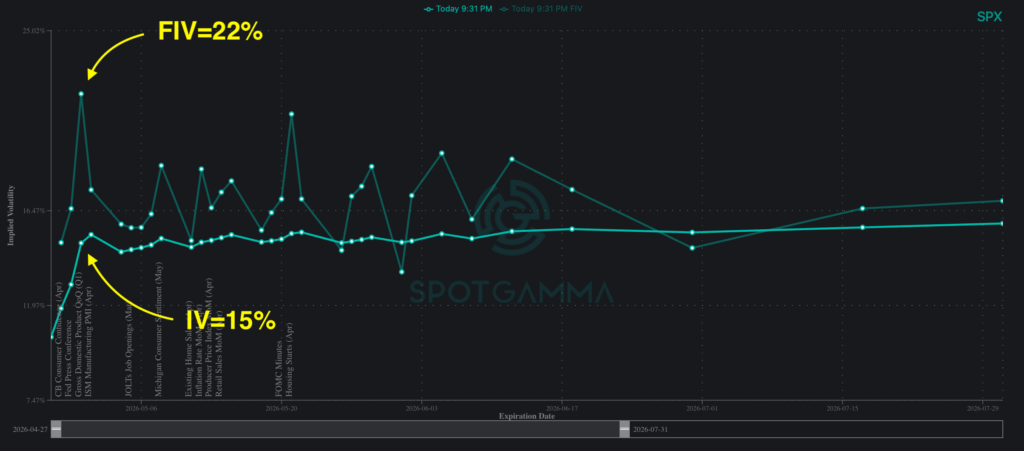

From the SPX volatility term structure, forward implied volatility into April 30 is at 22%, versus current implied volatility near 15%. This divergence suggests the options market may be underpricing post-event volatility following tech earnings and the FOMC decision.

These volatility dynamics point to potential event risk ahead. When implied volatility is low heading into high-impact events, options buyers might find more value than the surface-level numbers indicate.

The Call Build-Up: How Traders Are Positioning

In contrast to relatively low index volatility, traders appear to be buying volatility in individual names. In particular, last week’s institutional order flow points to broad optimism across the tech sector.

- Amazon (AMZN): ~6,600 June 220 calls, ~$30M in premium | Reports April 29, ~6% implied move

- Qualcomm (QCOM): ~25,000 December 200 calls, ~$13M in premium | Reports April 29, ~7% implied move

- Microsoft (MSFT): ~9,000 May 460 calls, ~$7M in premium | Reports April 29, ~6% implied move

- Alphabet (GOOGL): ~2,300 June 230 calls, ~$25M in premium | Reports April 29, ~5% implied move

One of the standout trades from our FlowPatrol report is ARM, which had unusual long-dated call buying last week. Roughly 2,000 Jan 2027 calls at 270 traded for $2.6M premium — and these contracts have gained 350% in value in just one week.

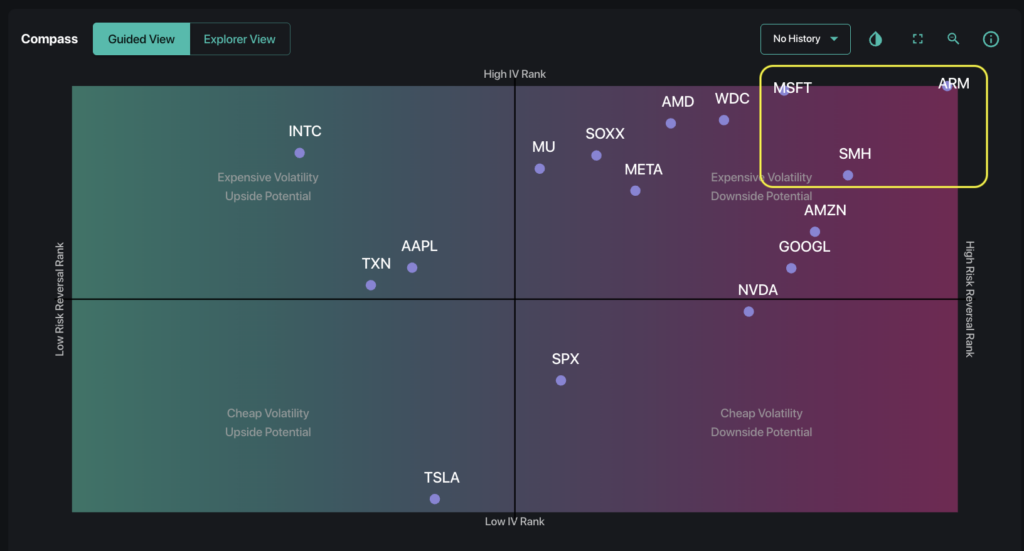

While index volatility looks subdued, single-name volatility tells a different story. Plotting the Mag7 alongside Semis on SpotGamma Compass Guided View shows these names clustered in the high IV Rank, high Risk Reversal quadrant — with ARM the most stretched of the group. The takeaway is: although we see consistent bullish flow from Tape, tech call options premiums are expensive now compared to the prior year’s values.

Convexity: Capitalizing on Outsized Movement

The key question is how to position for these dynamics, and the above mentioned ARM trade demonstrates the benefits of convexity. Convexity describes the nonlinear payout structure of options positions.

Here’s how convexity works in a trade: A long call’s maximum loss is capped at the premium paid. When a stock moves sharply beyond what the options market priced in, the gains can be dramatic. For example, when those OTM calls become ITM, and the delta expands from 25 to 50, the profits would more than double. That asymmetry is what makes convexity valuable heading into high-impact events.

As the below example of a MSFT May 460 call options shows using SpotGamma’s Options Calculator, traders can model payoff scenarios, including changes to implied volatility post-earnings, to better frame the risk-reward structure over time.

Post-OPEX volatility expansion has been kind to convexity strategies, allowing traders to risk relatively little capital for potentially large returns. The consistency of upside call buying suggests that institutional positioning is leaning into strength rather than fading it.

Call spreads and calendar spreads in particular may be of interest to take advantage of stock price movement post-earnings, while limiting the amount of upfront capital required.

When considering convexity trades, it’s critical to monitor the premium paid to ensure a favorable risk-reward. Tools such as SpotGamma’s Compass can help gauge how options are priced relative to recent history — helping you set more optimal trades with confidence.