Markets entered last week on fragile footing. In our previous Sunday note, we emphasized how negative dealer gamma, extreme put skew, and heavy 0DTE options activity set the market up for a trapdoor scenario. This created a market structure vulnerable to sharp drops and spikes in volatility, as we saw play out last week.

The dramatic escalation of the Iran crisis then injected a major geopolitical shock into an already delicate setup. Brent highlighted many of these risks during last Sunday’s livestream, which foreshadowed much of the market’s reaction.

While the S&P 500 had spent months consolidating within a tight range 6,800-7,000 range, that equilibrium quickly destabilized. A new market regime has taken hold, with a persistent geopolitical volatility premium capping market upside and threatening further volatility shocks. Until these risks subside, we remain in a risk-management market rather than a dip-buying environment.

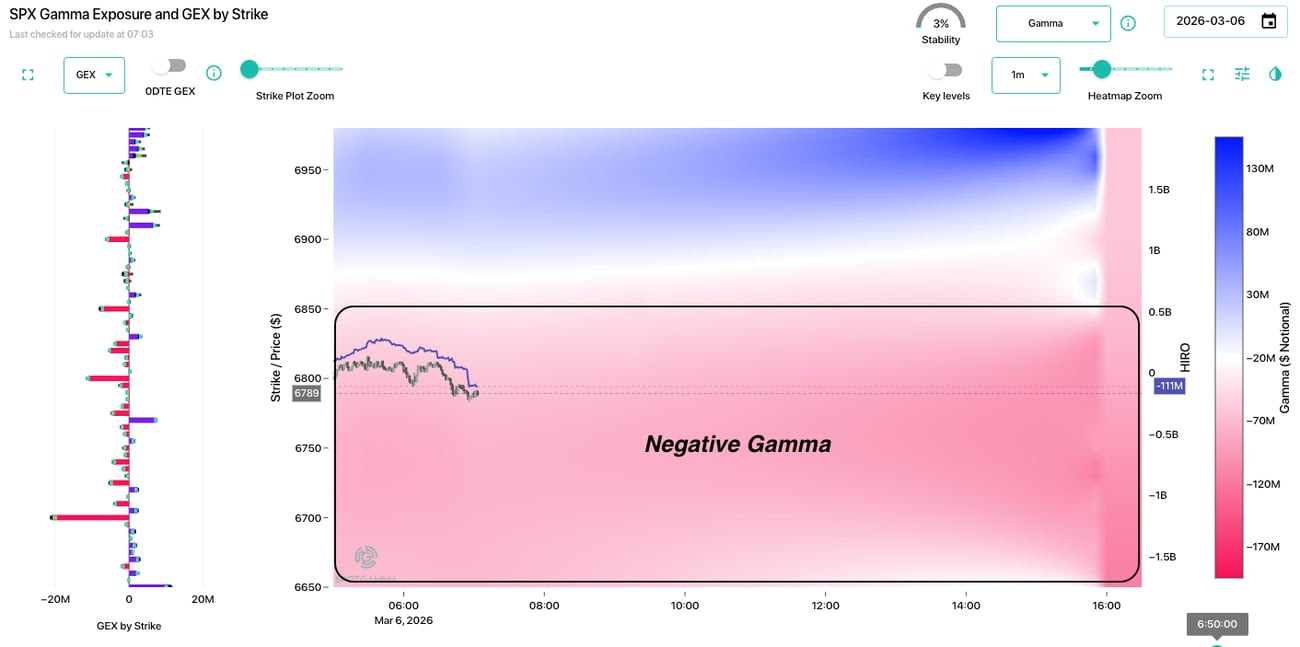

How did this new regime play out over the last week? The S&P 500 is down nearly 4% from all-time highs, falling below it’s previous 3-month range, while VIX spiked to nearly 30 as of Friday. SpotGamma’s TRACE chart above summarizes the core options market dynamic at play: negative gamma dominates the landscape below SPX 6,875.

The primary risk of negative gamma is that price movement becomes slippery in either direction, as dealers reinforce both rallies and selloffs by hedging with price action. We saw price bounce fluidly in this range all week, with daily open-to-close moves of 70-100 points each day.

As we mentioned in last Friday’s AM Founder’s Note: “The soft underbelly of this market remains in place”. Until positive gamma is re-established and the geopolitical volatility premium starts to come down, we remain on alert for larger intraday swings and day-to-day volatility.

Energy Sector Warning Signs: Oil Volatility Reaches Extremes

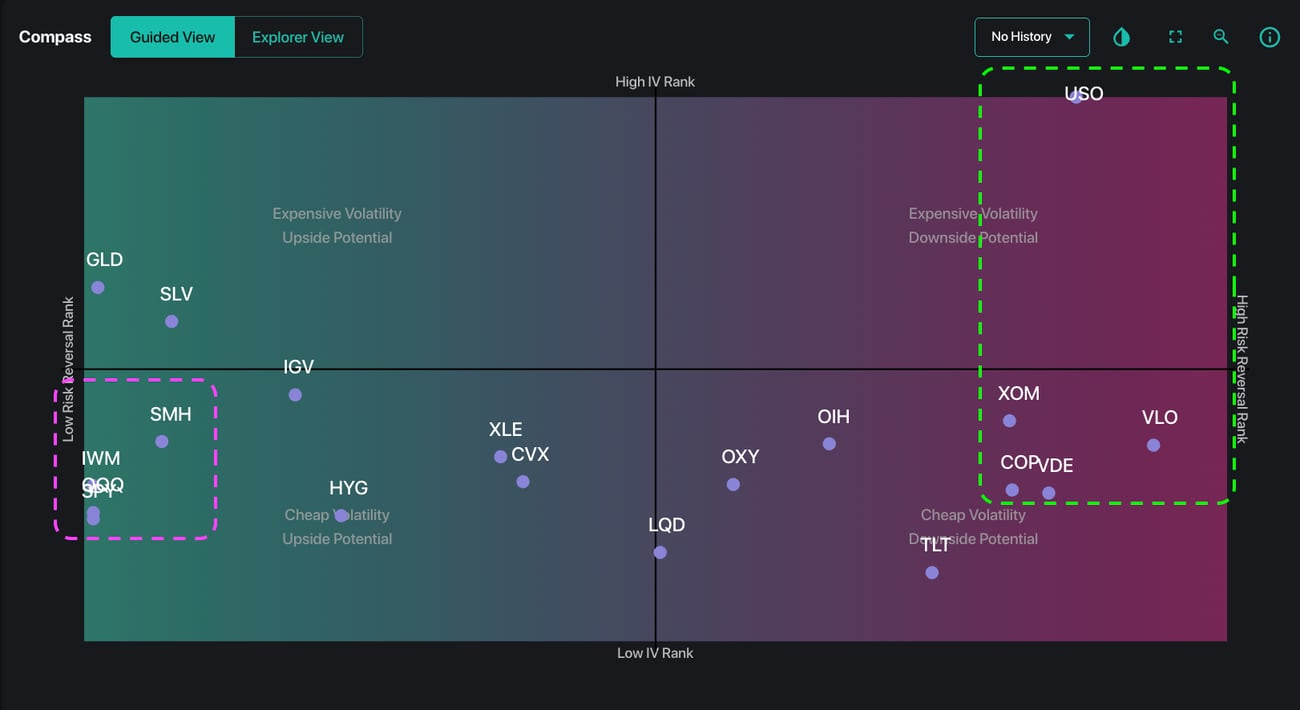

Amidst the new high-vol dynamics, energy markets may be flashing the most significant macro warning signals. Oil often acts as a leading volatility indicator for global risk assets. The surge in oil volatility suggests traders are pricing in the possibility of energy flow disruptions through the Strait of Hormuz.

As shown in the Compass chart below, the oil ETF USO currently sits at an IV Rank of 100%, meaning its implied volatility (and therefore options pricing) is now at the highest level recorded in the past year. Several energy-related tickers (USO, XOM, COP, VLO) also show elevated call skew readings — a sign that traders are yet positioning for further upside shocks in energy prices.

Forward Volatility: Market Hedges Against Further Downside

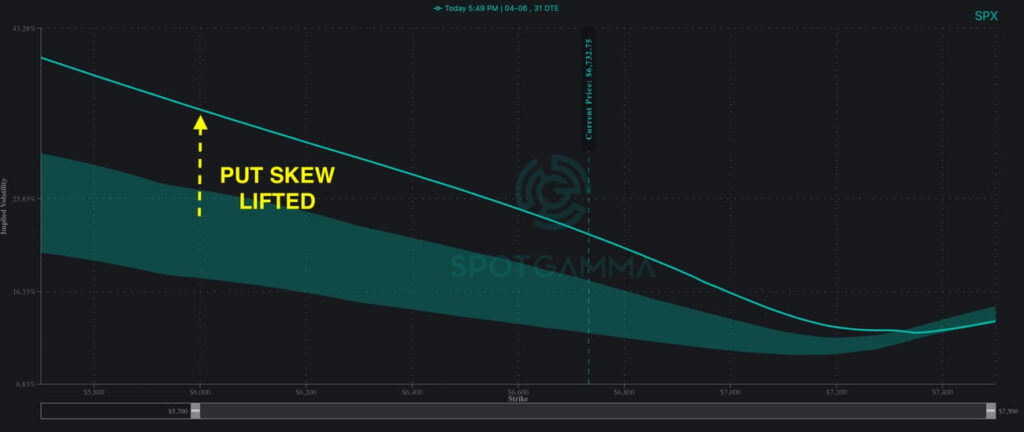

Perhaps most telling is how institutional money responded to last week’s selloff and price swings. For the past several months, dips below SPX 6,800 have been consistently bought, leading to sharp bullish reversals. However, these dynamics have reversed in the past week.

Instead of stepping in to buy the selloff, larger players appear to be hedging yet. SPX put skew has only increased, and elevated put demand suggests institutions are bracing for downside tail risk. When this type of hedging occurs alongside already elevated volatility, it can add further downward pressure and keeps vols elevated.

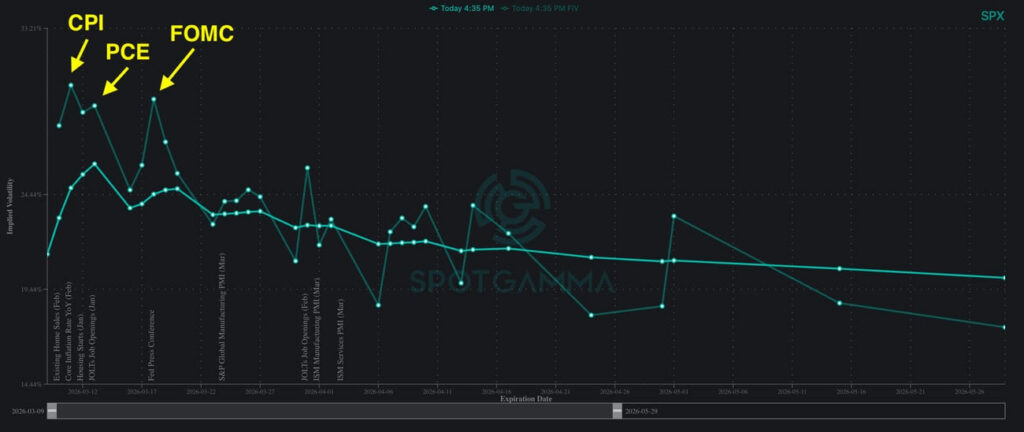

Looking ahead, there are three noteworthy events in the next two weeks that each carry a forward-IV premium:

- 3/11: CPI

- 3/13: PCE Release

- 3/18: FOMC

Although SPX implied volatility is already elevated, the spread between forward IV and current IV on the Term Structure chart implies additional risk of a volatility spike. Given the current environment, the options market may not be fully pricing in the potential jump risk around these macro events.

As we stated at the start of this note, we urge traders to think of the current environment as a “risk management” market. Further escalation or de-escalation of the Iran conflict will almost certainly impact the volatility premium weighing down major indices. SPX 6,875-6,900 forms the nearest tranche of upside resistance, while negative gamma dominates below. Staying informed of these dynamics, as they unfold, remains critical.