Despite a hawkish Fed rattling equities midweek, the market easily and quickly retraced any lost ground by Thursday. With June OPEX now behind us and implied volatility reset toward recent lows, there is a soft feeling of “what’s next?” for the S&P 500 until earnings season ramps up next month. The June FOMC meeting on […]

OPEX

Triple Witching + FOMC Fuels Volatility Risk

The market delivered several volatile sessions last week as traders navigated Wednesday’s CPI inflation report, Friday’s massive SpaceX IPO (SPCX), and a mix of Iran-driven headlines throughout. Last Sunday, we wrote about how extreme options positioning into major catalysts could spark the exact volatile market behavior observed over the past several days. Tuesday’s wild 200-point […]

The Hidden Mechanics Behind Last Week’s Rally

The S&P 500 has bounced back to record highs, closing decisively above 7,100 after Friday’s 1.2% rally. That marks a 12% rise from March lows in just under three weeks. In that same timeframe, volatility expectations have seemingly collapsed: VIX is down 40% since March 31, dropping from >30 to below 18. Crude oil has […]

Vol Crush Lifts the S&P 500 — Will the Rally Last?

Following last week’s ceasefire announcement, the S&P 500 lifted 3% from roughly 6,550 to 6,800. On the surface, this rally looked like a meaningful shift toward risk-on sentiment as implied volatility collapsed rapidly across all expirations. Similarly, VIX plummeted below 20 for the first time in four weeks, marking one of its largest single-day declines ever. Yet […]

How One Key Level Drove Last Week’s Rally

The S&P 500 bounced back 2% last week after scraping against 6-month lows. Mixed headlines on the Iran conflict explained much of this tug-of-war, yet markets are still holding their breath. For many traders, the rally felt counterintuitive: How can equities rally so furiously if geopolitical uncertainties remain unresolved? When looking at Tuesday’s major bounce in […]

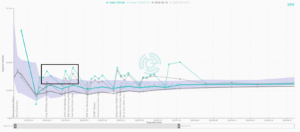

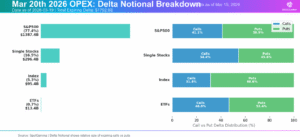

After OPEX: Market Loses Its Shock Absorber

The options market has just cleared one of the largest structural events of the quarter, as Friday’s OPEX saw nearly $1.4 trillion in delta notional expire for the S&P 500. Because significant positions have now rolled off from the March expiration, the market has lost an important stabilizing force just as macro pressures begin to build. […]

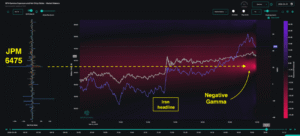

VIX Expiration, Oil, and the JP Morgan Collar Trade: What’s Driving the S&P 500

Market Summary The market is entering a critical window where VIX expiration, quarterly options expiration, crude oil, and the JP Morgan collar trade are all colliding at once. The core argument is simple: implied volatility remains elevated while realized volatility has stayed unusually muted, and that mismatch may not last much longer. If oil continues […]

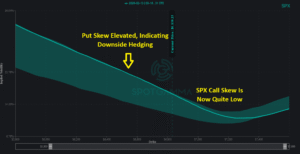

Right Tail Risk Is Building in the S&P 500

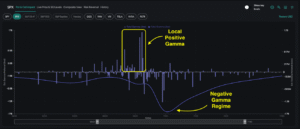

The market spent most of last week locked in the SPX 6,800–6,900 range that has largely held since Thanksgiving. Wednesday’s VIX expiration and Friday’s monthly OPEX defined the week’s rhythm, while negative gamma positioning and elevated single-stock put demand maintained pressure under the surface. Our historical OPEX data suggests the market is positioned for a […]

Flat Index Masks Hidden Chaos

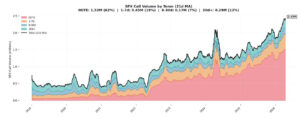

Overall price stability in the S&P 500 is masking one of the most unusual equity environments in recent years. While SPX has been roughly flat over the past month, the average constituent has moved 10.8% — a 99th percentile dispersion reading, as we discussed in our Thursday AM Founder’s Note. All signs point to increasing fragmentation beneath […]

The Market’s 0DTE Underbelly Is Exposed

Last week reminded us just how fast market stability can give way to volatility. After trading near all-time highs at 7,000, the S&P 500 fell 3% in just three sessions, closing Thursday at 6,798 amid weakness in software and crypto. Our last Sunday Newsletter focused specifically on how this type of fragility underscores today’s market. This […]