Fragility, Risk, and Potential Vol Reset

As the S&P 500 enters OPEX week, we echo the same theme of the past few weeks: this market remains fragile. Last week’s selloff pushed the index below the three-month trading range of SPX 6,800-7,000 that had held since late 2025, subsequently closing down 5% since mid-January. The conflict with Iran continues to escalate, shaping headline news and sending shocks throughout the market.

In light of recent market volatility, we focus on expiration dynamics specifically: these cycles often can reverse the market’s trends and volatility patterns. The week ahead features monthly VIX and SPX expirations, followed shortly afterwards by quarterly OPEX. The key question now is whether this Triple Witching will reset volatility and stabilize conditions, or open the door to an even more precarious regime.

Gaps Widens Between Implied and Realized Volatility

We have written previously about how SPX put skew has been elevated, while overall IV remains somewhat muted (SPX IV Rank = 31%). In other words, traders have been paying up for tail protection.

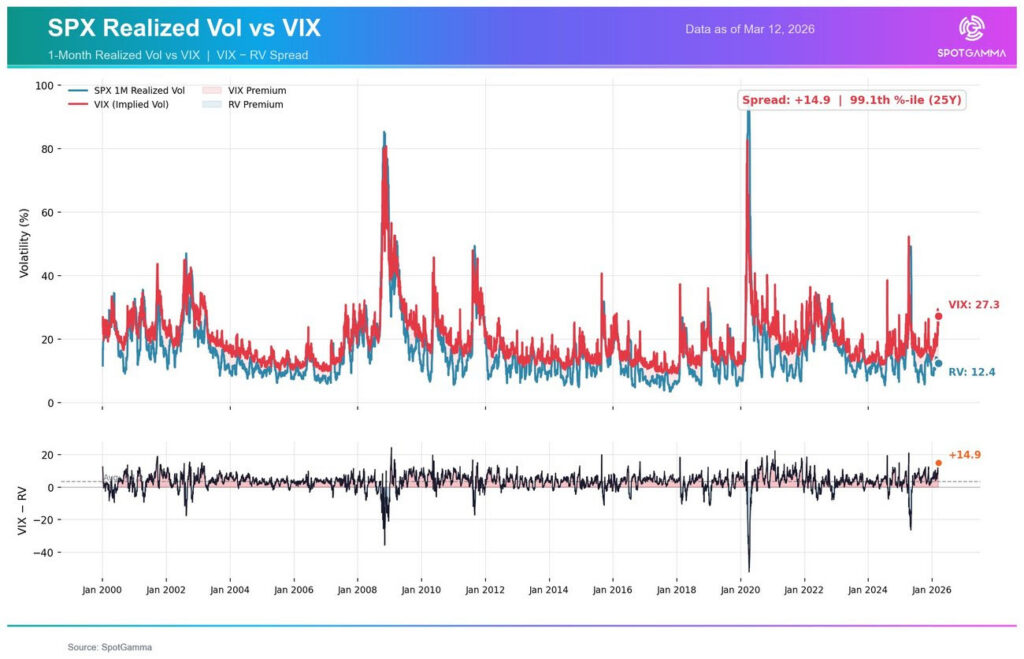

One key tension in this market is the large discrepancy between the VIX and SPX realized volatility. As shown in the chart below, VIX usually maps +5 pts above 1-month RV. As of this past Thursday, that gap measured as high as +14.9 pts — and a gap of this size does not typically last long.

The tension between the VIX and realized creates an unstable equilibrium: either VIX is pushed lower as markets stabilize, or realized volatility expands quickly to catch up. This gives us the distinct feeling that one way or another, something’s got to give.

Negative Gamma Leads to “Squeeze Risk”

One argument in favor of the vol spike scenario is the persistence of the negative gamma regime for SPX. The TRACE heatmap below shows red virtually everywhere, equating to negative dealer gamma. When dealers hold negative gamma, they hedge by selling into declines and buying with rallies, amplifying price movement.

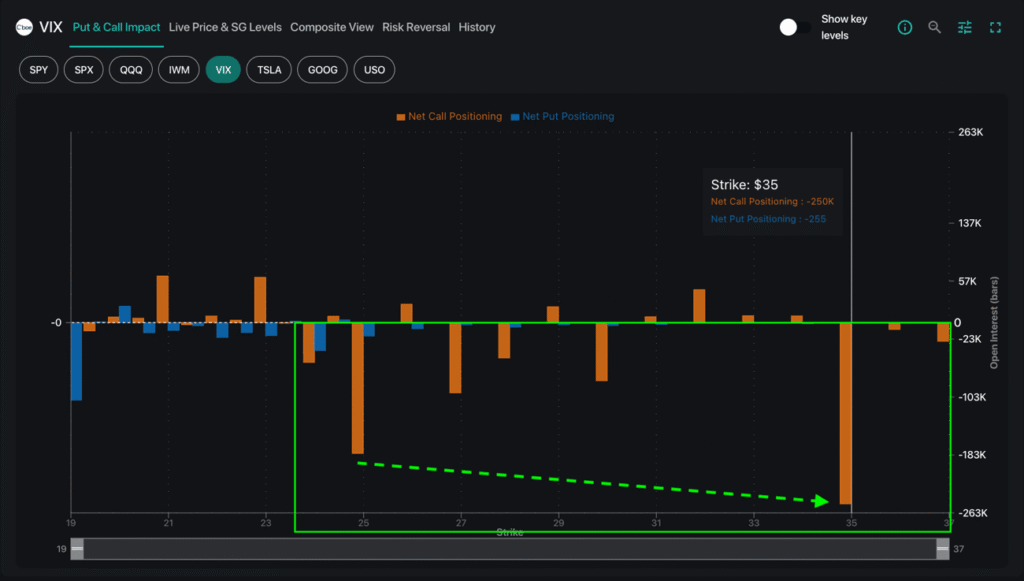

A similar dynamic is developing in VIX positioning: dealers appear to be cumulatively short gamma across the board. The VIX 35 level stands out in particular, as dealers are short ~250k calls at that strike. As VIX closed last week above the Key Gamma Strike (support) at 27, a sustained move higher could bring about squeeze conditions.

With markets facing continued downward pressure, this risk is that negative gamma could force a “spot dip, vol rip” scenario for the S&P 500.

Friday’s OPEX: Tipping Point or Turning Point

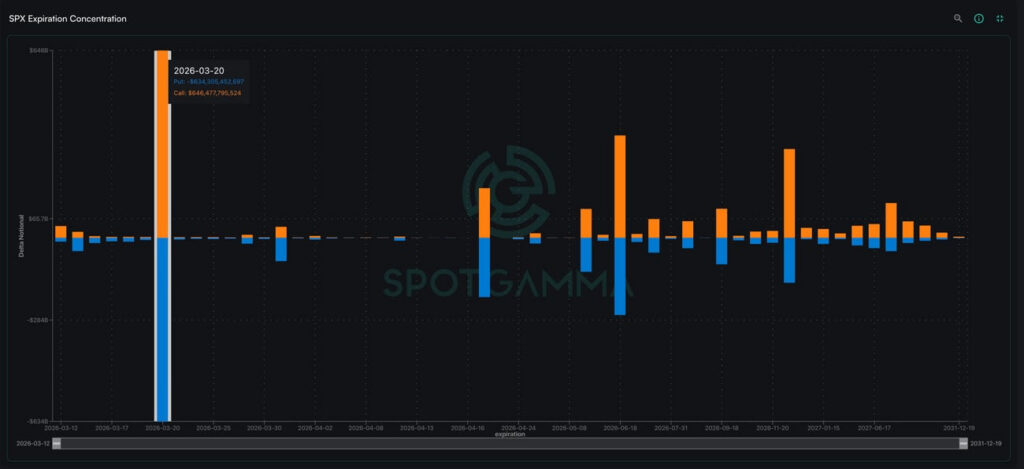

The March monthly expiration stands out as particularly important. Friday’s OPEX represents one of the the largest expirations on record with roughly $1.3 trillion delta notional — about 30% of total market exposure — set to roll off.

Positioning is also relatively balanced with a nearly perfect 50-50 split between calls and puts. Directional impact may heavily depend on how traders choose to reposition following this expiration.

The most significant structural factor to monitor is the JPM Collar position. This quarter, the collar consists of 35,000 contracts on an SPX 5,470 / 6,475 put spread with a short call at the 7,155 strike.

That structure expires at the end of March, and we expect a meaningful impact from dealer repositioning following the roll of the JPM Collar. As a result, quarterly expiration on March 31 remains a key date to watch for unusual options-driven dynamics.

Taken together, the Triple Witching OPEX makes for one of the most significant events of the past few months. Depending on trader repositioning flows, this could serve as the turning point for stabilizing conditions, or tip the market into more volatility yet. This week also brings FOMC (3/18), creating yet another key date to watch.

With negative gamma dominant, skew elevated, and expiration dyamics ahead, the quiet range-bound market has now disappeared. We encourage our readers to monitor option flows surrounding the upcoming events, watch for headlines, and stay nimble.