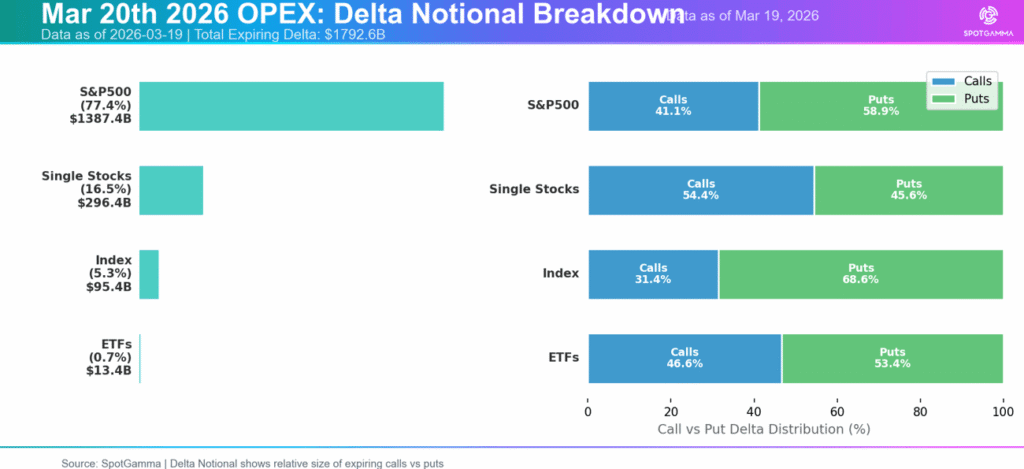

The options market has just cleared one of the largest structural events of the quarter, as Friday’s OPEX saw nearly $1.4 trillion in delta notional expire for the S&P 500. Because significant positions have now rolled off from the March expiration, the market has lost an important stabilizing force just as macro pressures begin to build.

Even in the best case scenario, this tell us that we’re not out of the woods yet. The worst case scenario tells us to hold on tight.

The loss of stabilizing positioning from March OPEX comes at a particularly precarious moment. SPX has broken below the 6,600 Put Wall, closing Friday at 6,506 and now down over 7% from January highs. These dynamics may finally put the nail in the coffin on the range-bound environment we observed at the start of 2026.

The macro factors of concern include continued global conflict, elevated oil prices, and shifting rate cut expectations following FOMC. Any rally at this point would likely require one or all of those market stressors to ease to meaningfully lift equities.

At least through quarter-end, major indices appear increasingly susceptible to larger directional moves. While this volatility could manifest in terms of dramatic upside as well as downside, heightened put skew indicates that traders are largely hedging against the threat of a continued selloff.

Realized Volatility Has Room to Expand

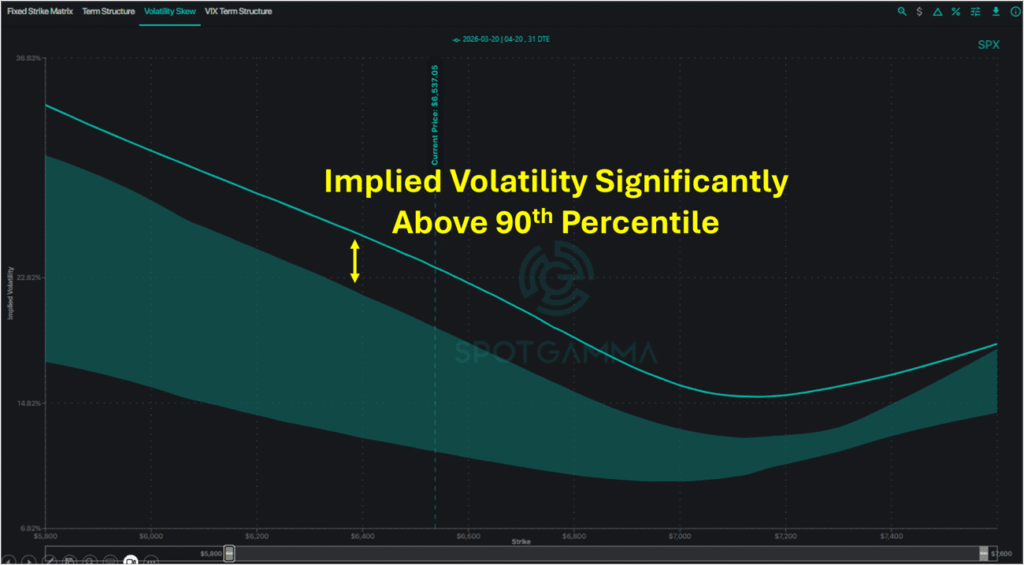

A look at market volatility reveals that things remain turbulent. Although SPX implied vol eased somewhat after March OPEX, that decline looks more like the removal of near-term event premium than any sort of return to calm. Options are still quite expensive compared to the period immediately before the Iran conflict, suggesting traders remain unwilling to short options with confidence.

At the same time, downside hedging demand is rebuilding. SPX put skew steepened again over the past week, showing that large traders are reloading puts rather than shifting toward calls. This is concerning, as SPX is already down over 7% from recent highs, yet traders continue to pay for protection rather than position for recovery.

The worry is that realized volatility still has room to rise and “catch up” with implied volatility. In previous periods of market stress, that kind of gap has often closed through realized vol grinding higher, especially after major expirations and following the breach of key support levels.

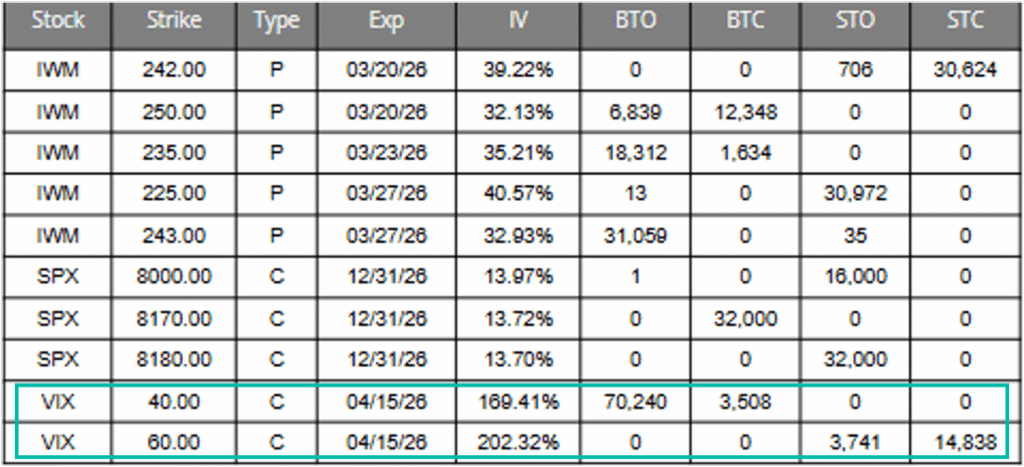

Trader VIX positioning further indicates the threat of volatility. On March 19, SpotGamma’s FlowPatrol flagged roughly 70,000 April 40 VIX calls traded in a single session — a sizeable upside volatility bet. Trades like this suggest that at least one large participant is preparing for a sharp rise in SPX implied volatility, which often accompanies fast equity drawdowns.

If VIX begins to move higher, those far out-of-the-money calls could also force dealers to hedge in ways that reinforce further SPX volatility expansion.

What Happened to the “Safe Haven” Assets?

Recent cross-asset behavior confirms a broader de-risking dynamic. Traditional “safe haven” assets such as bonds and metals declined alongside equities, signaling that investors are reducing overall exposure rather than rotating into safety.

Diving into metals specifically, GLD fell sharply last week along with the market. Gold is now down 10% from Monday’s open and over 15% in the last three weeks.

A look at GLD volatility reveals that the ETF is highly skewed towards puts, with 99th percentile put skew and 1st percentile call skew. This lopsided dynamic suggests aggressive downside hedging and broad deleveraging from traders.

At this point, some readers may be wondering: “What does gamma tell us about the market? Does dealer hedging not matter right now?”

Of course, dealer hedging remains an important factor: we are focusing less on this dynamic at present because negative dealer gamma has now persisted for weeks. Until traders begin to more aggressively sell options — forcing market makers into long gamma positions — price action is expected to remain fluid as dealers sell into dips and buy into rallies.

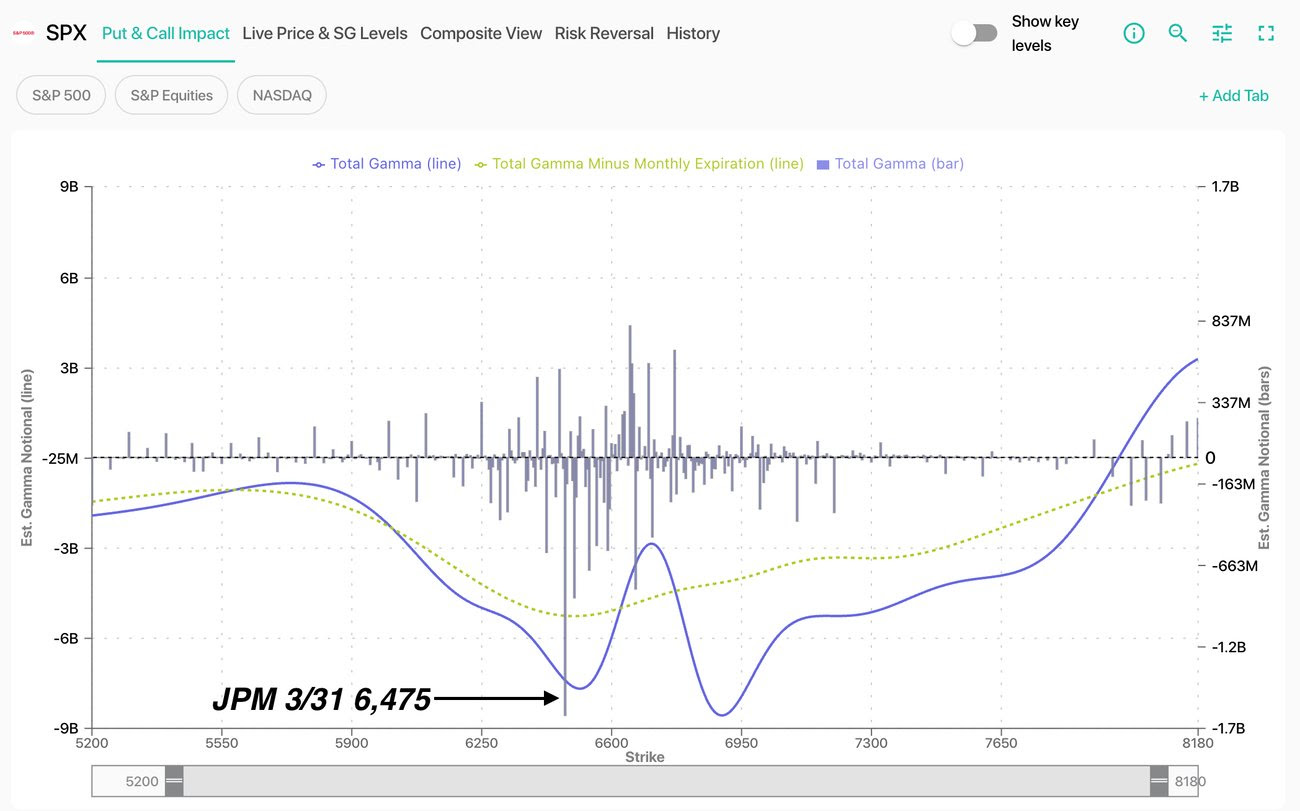

Last week’s expiration cleared significant positions from the table, and quarterly OPEX may bring the JPM Collar’s 6,475 put strike into play as a key reference point into month-end. However, with that structure set to expire on March 31, any impact from this massive position may prove to be short-lived.

Between expiration dynamics, put skew rebuilding, and persistent negative gamma, the ingredients are in place for a more dynamic — and potentially more volatile — market in the coming weeks.

Stay nimble, stay hedged, and let the data lead the way.