The AI trade has been the story of the first half of 2026, and semiconductors have been the main characters. The sector now accounts for roughly 20% of the entire S&P 500 — a historically high concentration. As we covered in our previous newsletter, any meaningful profit-taking in this area brings up the important question of where that capital rotates next.

Last week, we broke down options dynamics with the healthcare sector serving as a primary target for trader rotation. This week, we’ll discuss the software sector and how traders could identify and trade candidates in the space.

Zooming out, the market backdrop is deceptively calm: major indices have ground steadily higher all year, with SPX posting a solid 9% YTD return. Beneath the surface, however, we see dispersion has been a defining feature: top-performing AI names have risen dramatically, now showing extreme call skew as traders rush to capture further upside.

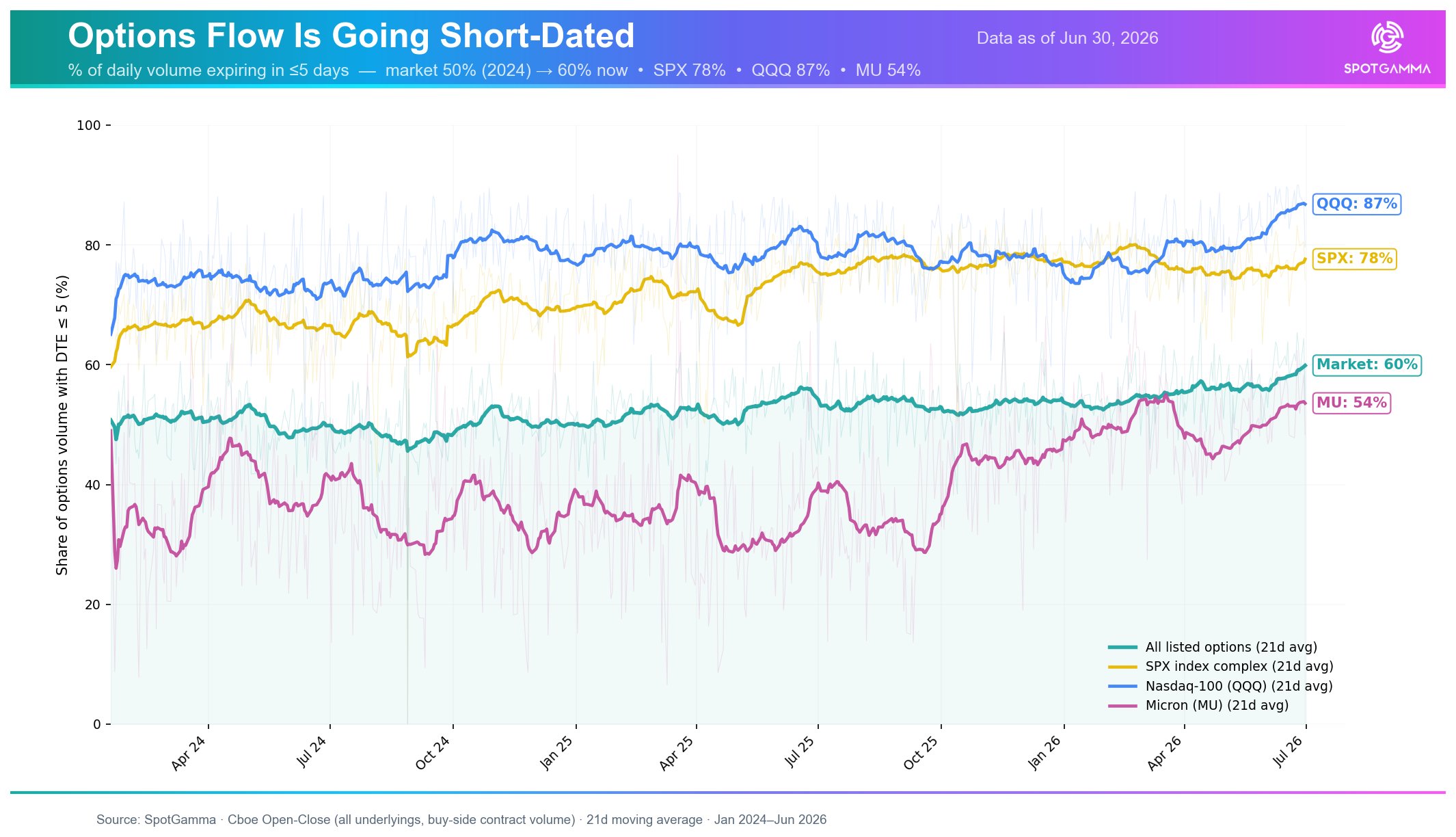

The growing, market-wide influence of options has established new ways to trade capital rotations. Short-dated contracts now dominate the options market, with 87% of QQQ options volume and 78% of SPX options volume trading with fewer than five days to expiration. That concentration reflects increasingly tactical positioning, allowing traders to rapidly adjust exposure.

This trend accelerated following the introduction of Monday and Wednesday expirations for single-stock options in certain stocks earlier this year. This short-term options activity increasingly influences price action via dealer hedging, as options market dealers must more aggressively hedge shorter-dated exposure.

The Stock Pickers’ Market

The dispersion beneath the calm index is striking. Memory names such as Micron (MU, +200% YTD) and SanDisk (SNDK, +514% YTD) have delivered exceptional returns. At the same time, several marquee software names have lagged significantly: Microsoft (MSFT) has dropped 18% YTD, while ServiceNow (NOW) is down 28%.

Last week, however, the market began to show signs of the capital rotating. The semiconductor ETF (SMH) declined 4%, while the software ETF (IGV) gained 10%. One week does not establish a trend, and sector rotations can reverse just as quickly as they emerge. Is this simply an oversold bounce, or the beginning of a broader rotation?

To help answer whether this rotation can develop into something more durable, we look beyond price alone to focus on options positioning. Using the SpotGamma Compass and Equity Hub, we screened software names trading near SpotGamma Key Levels. This gave us a view of implied volatility, call versus put skew, and dealer gamma positioning.

From that shortlist, several names stood out with compelling risk-reward attributes. ServiceNow (NOW) in particular displayed several interesting characteristics, which we can dive into to explore potential trade opportunities.

Trading NOW: Structures that Make Sense

ServiceNow (NOW) presents interesting dynamics across both volatility metrics and options positioning. The stock currently exhibits a quite balanced profile with a call skew of 28% and a put skew of 20%. When evaluating call and put skew, SpotGamma typically compares the difference between 50 delta and 25 delta options — suggesting low demand for out-of-the-money options in NOW compared to near-the-money strikes.

Notably, NOW also has an IV Rank of 91% — which means individual options contracts have grown expensive. Traders have bought up options in the name, but without an emphasis on the tails.

The dealer gamma positioning for NOW adds another interesting dimension to the setup. Dealers hold positive gamma between 75 and 100, meaning hedging flows may help dampen volatility and stabilize pullbacks. Above 100, this positioning shifts to negative gamma — creating the potential for hedging flows to amplify any upward breakout.

When combined with SpotGamma Key Levels, the Key Gamma Strike at 110 provides a logical framework for structuring a bullish trade. Given more expensive prices, call spreads may be a more capital efficient way to structure the upside exposure.

One example would be the August 110/130 call spread shown above, which currently offers approximately a 2:1 reward-to-risk profile. While the trade itself uses August expiration to avoid theta decay, the short-dated flows could be the force that drives the day-to-day hedging pressure.

Timing becomes an important consideration: ServiceNow reports earnings on July 22, creating a binary event that could easily create a meaningful decline in implied volatility following. As a result, this setup could be viewed as a momentum trade ahead of earnings rather than one intended to carry through the event. More complex structures — such as call diagonals — could attempt to capture this decline.

The semiconductor-to-software rotation is one story worth watching through the second half of 2026. To discover and capitalize on opportunities, certain criteria may make some names stand out: supportive dealer positioning below, the potential for accelerated flows (negative gamma) to the upside, and pricing that has yet to fully reflect renewed investor interest.