Despite a hawkish Fed rattling equities midweek, the market easily and quickly retraced any lost ground by Thursday. With June OPEX now behind us and implied volatility reset toward recent lows, there is a soft feeling of “what’s next?” for the S&P 500 until earnings season ramps up next month.

The June FOMC meeting on Wednesday afternoon delivered a surprise with the “dot plot” shifting decisively higher. Bond traders were fully pricing in a rate hike by October following Chairman Warsh’s first press conference, with equities selling off as short-term yields spiked.

What’s notable, however, is just how quickly the equity market absorbed any selling pressure. By Thursday, stocks had recovered much of the decline.

The mechanism behind that rebound is precisely what should give traders caution: volatility sellers stepped in aggressively in front of the three-day weekend, and mechanical volatility compression provided tailwinds for the market. The result was a reset of SPX implied volatility back toward recent lows.

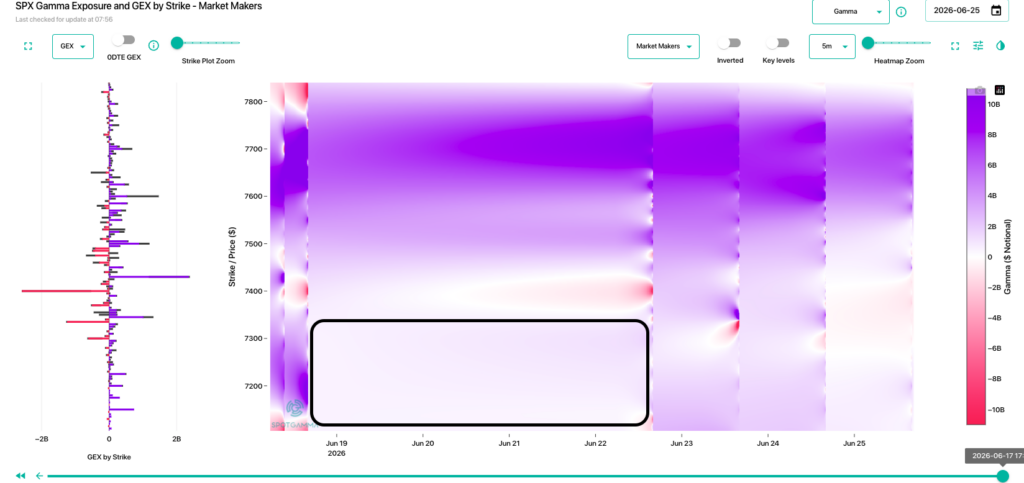

From our TRACE heatmap, we can see that positive dealer gamma below the current SPX price becomes much more mild into the upcoming week. This suggests traders were willing to sell short-dated options, but that conviction did not extend into longer-dated expirations.

The reduction in supportive positive gamma to the downside means the market cannot rely on stabilizing dealer flows should price begin to drop.

On Monday, we will be watching to see whether traders sell OTM puts to once again establish a positive gamma regime. Alternatively, we may anticipate more fluid price action should dealer gamma exposure remain neutral.

SPCX’s Options Debut Runs Hot

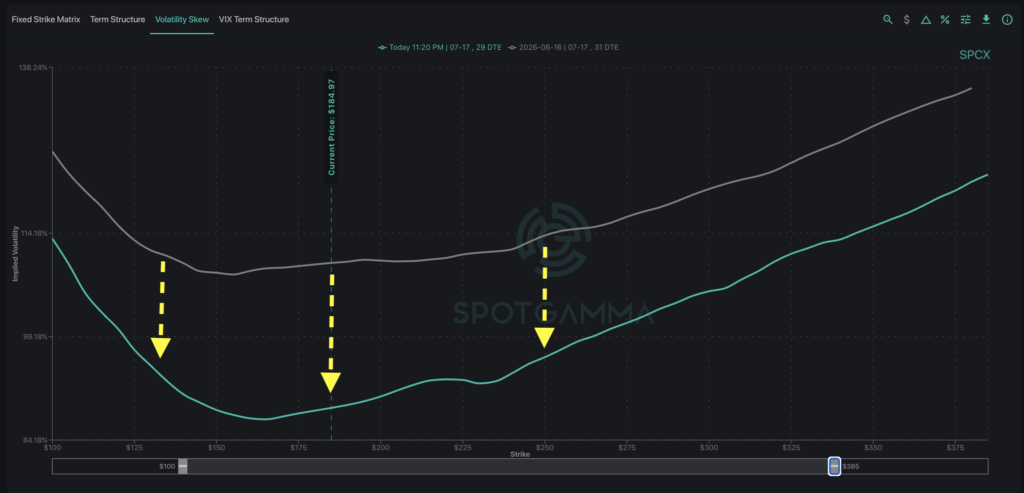

Tuesday’s launch of SpaceX (SPCX) options has proven to be a development worth monitoring, with the stock immediately ranked among the top 10 actively traded options products. Early contracts carried elevated implied volatility, particularly for the June 18 weekly expiration, as traders aggressively purchased calls to partake in the post-IPO frenzy.

SPCX options trading remains heavily skewed toward calls, suggesting investors are paying a premium for upside participation rather than simply hedging downside risk.

The July volatility surface, however, tells a slightly different story. Implied volatility for the monthly expiration declined sharply between Tuesday and Thursday, with at-the-money IVs dropping 20 vol points from 110% to 90%. This suggests the market expects the initial speculative momentum to stabilize and volatility to normalize.

For now, the excitement around SPCX appears to be at least somewhat fading. However, with potential inclusion in major indices such as the Russell and Nasdaq in the coming weeks, the volatility experienced in SPCX could expand to the index level.

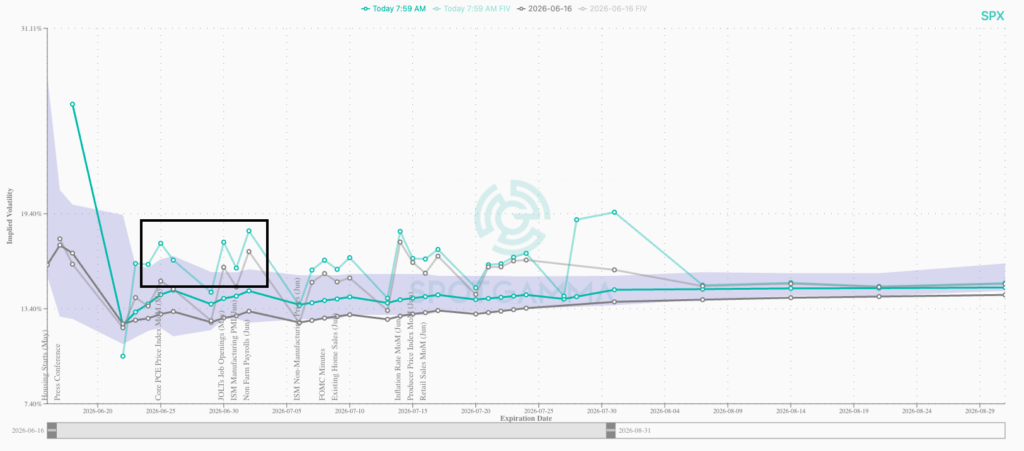

What’s Ahead: MU, PCE, and the JPM Collar

With FOMC, OPEX, and the SPCX IPO now behind us, the calendar has cleared considerably. Three particular upcoming catalysts are worth flagging: Micron earnings (June 25), PCE inflation data (June 26), and the JPM Collar roll (June 30).

For MU, the options market is currently pricing in an implied move of ~12% out of earnings. Traders are likely looking for the outsized returns from last month’s AI earnings run to continue, and Micron may set the tone for the broader AI trade.

PCE inflation data follows on June 26, which has traditionally provided the Fed’s preferred inflation gauge. This release gives us an important read on whether price pressures are likely to ease.

The JPM Collar roll arrives on the last day of the quarter, with the short call strike near SPX 6,900 serving as the nearest leg. While it would take a sizeable selloff to reach that level, this strike could act as a price magnet given a large enough drop — providing noteworthy negative gamma to the downside.