The following is a guest post from Doug Pless. As I discussed previously, I begin my morning preparation by reading the SpotGamma AM Report when I plan to trade futures. For ES futures, I note gamma levels, the SpotGamma Index, and Gamma Notional for SPX and SPY. The SpotGamma Gamma Index is a proprietary measurement […]

vanna

When YOLO goes “YOL-Oh No!”

Summary: Issue: SpotGamma believes that current markets reflect a great amount of risk and face the prospect of a violent drawdown. This is due to the following: Hedging: Low levels of options-based hedging. Short-Selling: Low levels of stock shorting. Speculation: High levels of margin used to buy stocks. Remedies: SpotGamma levels continue to be […]

SpotGamma 1/18/21

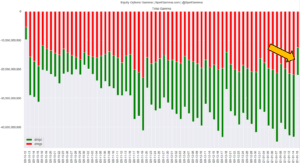

We noted to subscribers on Thursday & Friday that we thought markets were entering a period with the potential for high volatility. This was due to Friday’s very large 1/15 options expiration which resulted in a ~50% reduction in single stock gamma as seen below. This creates volatility because as large options positions expired, are […]

“Full-Tilt Insanity Mode” – Nomura Warns This Week’s OpEx Is “Absolutely Going To Matter” For ‘Weaponized Gamma’ Crowd

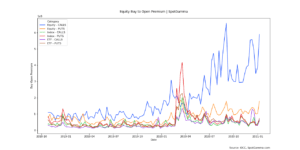

Via ZeroHedge The world appears to be stock in what Nomura’s Charlie McElligott calls “Robinhood / YOLO / ‘weaponized gamma’” nonsense as the equity buy-to-open premium is soaring in individual stocks (and indices)… Source: SpotGamma Specifically, the Nomura MD notes that it is Op-Ex week, and the options positioning is absolutely going to matter, particularly off the back of […]

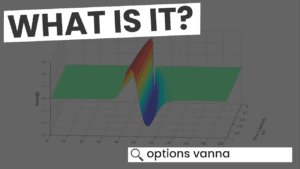

Options Vanna

There is a lot of talk recently about options Vanna and we wanted to address some of these points here. The basic concept as applied to our SPX/SPY models can be distilled to this: • When implied volatility (i.e. VIX) declines stocks go up• When implied volatility increases stocks go down Obviously there are many […]

Options Vanna Rally

Now a prescient time to talk about options Vanna, and a Vanna rally. Vanna measures the change in delta for a change in Implied Volatility. Long calls + short puts = Long Vanna We view options market makers as typically long vanna. When volatility crushes they therefore must buy stock back to reduce their hedges. […]