Over the past several weeks, we have consistently highlighted the market’s growing fragility. From the negative gamma “trapdoor” to the destabilizing impact of geopolitical shocks, the message has been clear: this is no longer a range-bound market. Last week confirmed those warnings, as the S&P 500 is down nearly 9% from all-time highs. On Thursday and Friday, traders […]

VIX

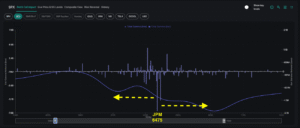

After OPEX: Market Loses Its Shock Absorber

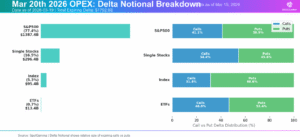

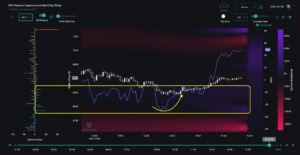

The options market has just cleared one of the largest structural events of the quarter, as Friday’s OPEX saw nearly $1.4 trillion in delta notional expire for the S&P 500. Because significant positions have now rolled off from the March expiration, the market has lost an important stabilizing force just as macro pressures begin to build. […]

VIX Expiration, Oil, and the JP Morgan Collar Trade: What’s Driving the S&P 500

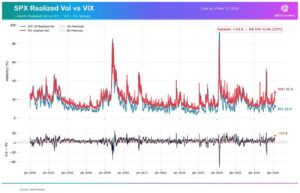

Market Summary The market is entering a critical window where VIX expiration, quarterly options expiration, crude oil, and the JP Morgan collar trade are all colliding at once. The core argument is simple: implied volatility remains elevated while realized volatility has stayed unusually muted, and that mismatch may not last much longer. If oil continues […]

March OPEX: Tipping Point or Turning Point?

Fragility, Risk, and Potential Vol Reset As the S&P 500 enters OPEX week, we echo the same theme of the past few weeks: this market remains fragile. Last week’s selloff pushed the index below the three-month trading range of SPX 6,800-7,000 that had held since late 2025, subsequently closing down 5% since mid-January. The conflict with Iran continues […]

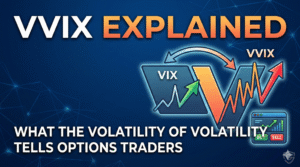

VVIX Explained: What the Volatility Index Tells Traders

The VVIX measures the expected volatility of the VIX itself — giving options traders a window into hedging demand, dealer positioning, and what the market is pricing before volatility materializes. SpotGamma’s forward return data shows

what elevated VVIX levels have historically meant for SPY and VIX.

Flat Index Masks Hidden Chaos

Overall price stability in the S&P 500 is masking one of the most unusual equity environments in recent years. While SPX has been roughly flat over the past month, the average constituent has moved 10.8% — a 99th percentile dispersion reading, as we discussed in our Thursday AM Founder’s Note. All signs point to increasing fragmentation beneath […]

The Market’s 0DTE Underbelly Is Exposed

Last week reminded us just how fast market stability can give way to volatility. After trading near all-time highs at 7,000, the S&P 500 fell 3% in just three sessions, closing Thursday at 6,798 amid weakness in software and crypto. Our last Sunday Newsletter focused specifically on how this type of fragility underscores today’s market. This […]

SPX Touches 7,000 and Cracks — What Makes This Market So Fragile?

Market Fragility in the Face of All-Time Highs As the S&P 500 pushes record highs, the options market continues to flash warning signals beneath the surface. Underlying risk from volatility discrepancies and index-equity correlation suggest an environment prone to vol spasms — similar to what we witnessed with Thursday’s (1/29) sharp selloff and reversal. These […]

Vanna Fuels Market Rally as Market Fears Subside

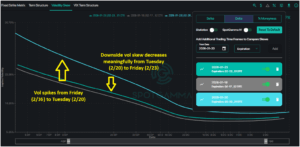

Last week began with fear dominating market sentiment: analysts widely attributed Tuesday’s 2% SPX selloff to Greenland worries and tariff threats. As we pointed out in last weekend’s newsletter, traders had begun hedging against downside risk as put skew increased and volatility premiums rose. However, the quick turnaround back to SPX 6,900 seemed to erase any […]

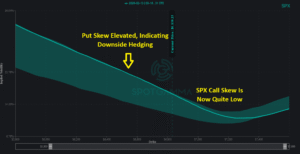

Defensive Positioning Emerges as Market Rallies

Traders Turn Defensive In the Face of Market’s Climb SPX tested fresh all-time highs last week, with positive gamma providing guardrails for the broader market. In the face of headline noise—from criminal investigations into Powell to Iran-related escalation—the market absorbed every dip, with the 6,890 Risk Pivot level from Monday’s AM Founder’s Note holding firm. However, increasing put skew and […]